9. Gaussian Processes#

The purpose of this notebook is to provide an introduction to Gaussian Processes (GPs) and its main properties.

Before diving into the theory, let’s start by loading the libraries

matplotlib

together with the style sheet Quant-Pastel Light.

These tools will help us to make insightful visualisations.

9.1. Introduction#

In probability theory and statistics, a Gaussian process is a stochastic process, such that every finite collection of those random variables has a multivariate normal distribution. The distribution of a Gaussian process is the joint distribution of all those (infinitely many) random variables, and as such, it is a distribution over functions with a continuous domain, e.g. time or space.

The concept of Gaussian processes is named after Carl Friedrich Gauss because it is based on the notion of the Gaussian distribution (normal distribution). Gaussian processes can be seen as an infinite-dimensional generalization of multivariate normal distributions.

Gaussian Processes (GPs) are one of the most elegant ideas in probabilistic modelling: instead of learning parameters, we learn a distribution over functions. They are widely used in:

Regression

Bayesian Optimisation

Spatial Modelling

Uncertainty Quantification

9.2. Definition#

A Gaussian Process (GP) is a stochastic process \(X = \{X_t : t \in \mathcal{T}\}\) where \(\mathcal{T} \subseteq \mathbb{R}^d\), such that for every finite set of indices \(\{t_1, \cdots, t_n\}\) in the index set \(\mathcal{T}\), the random vector

has a multivariate Gaussian distribution, with mean and covariance given by

That is

A Gaussian Process (GP) is then fully specified by two functions, namely

a Mean function \(m(t) = E[X_t]\)

a Covariance function \(k(t, s)= E[(X_s- E[X_s])(X_t- E[X_t])]\)

where the covariance function must be symmetric, and positive semi-definite, i.e. for any finite \(\{t_i\}\) and \(\{c_i\} \subset \mathbb{R}\):

Hereafter we are gong to use the notation \(X \sim \mathcal{GP}(m, k)\).

Note

The covariance function \(k(t, s)\) is often called kernel function

A GP is called centered if \(m(t) = 0\) for all \(t \in \mathcal{T}\)

Theorem. A stochastic process \(X = \{X_t : t \in \mathcal{T}\}\) is a Gaussian process if and only if every finite linear combination of its values is a Gaussian random variable.

The linear combination characterisation is very useful in practice because:

It reduces checking joint Gaussianity to checking scalar random variables

It makes closure properties immediate: sums, differences, and integrals of GP-distributed processes are again Gaussian

It directly motivates the kernel/covariance structure as the object controlling the variance of every possible projection \(c^{T} X\)

9.2.1. Marginal Distributions#

By definition, the marginal distributions of a Gaussian process are Gaussian. That is, for any \(t \in \mathcal{T}\), the random variable \(X_t\) is Gaussian with mean \(m(t)\) and variance \(k(t, t)\):

9.2.2. Examples#

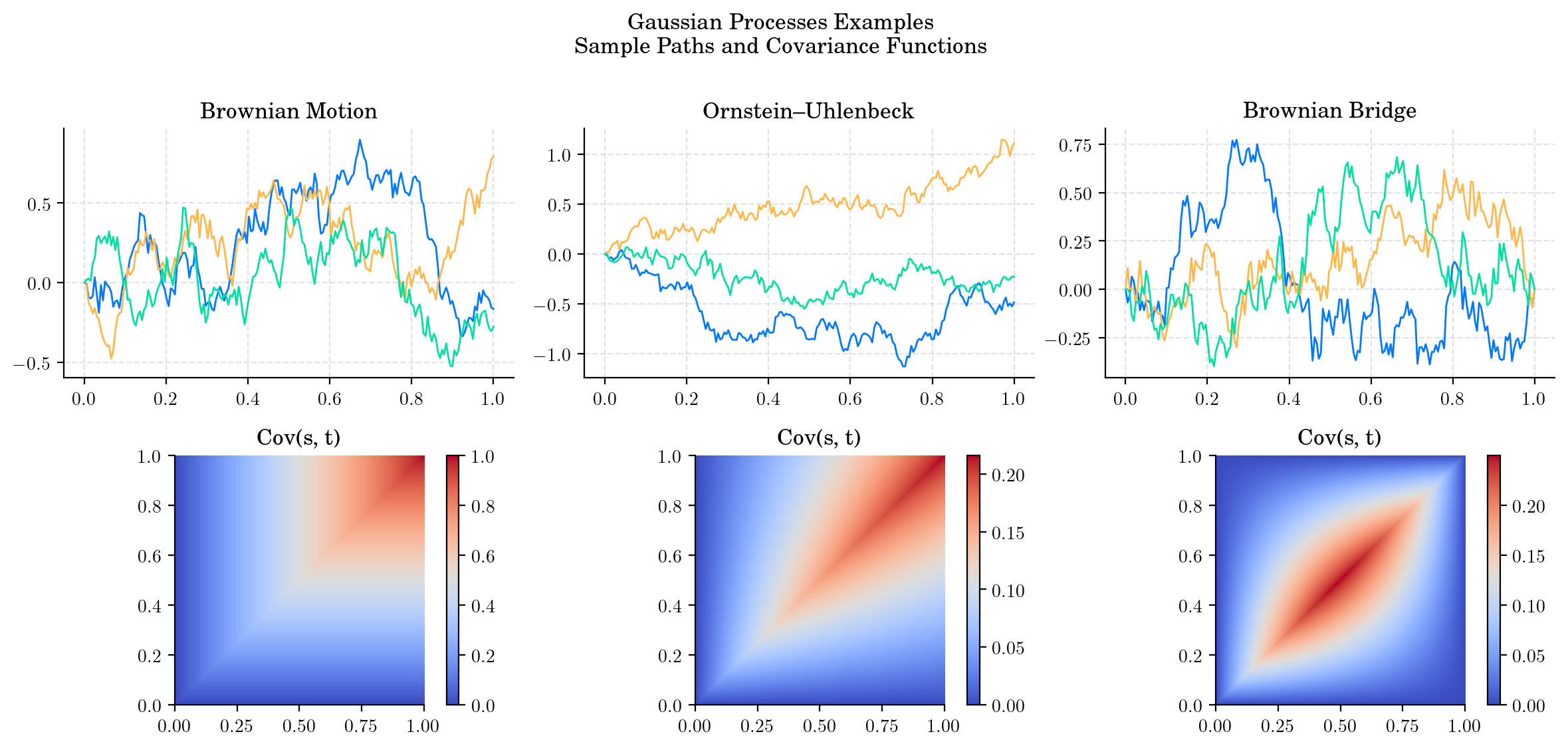

A Brownian motion \(W = \{W_t : t\geq 0\}\) is a centered GP with covariance function

An Orstein-Uhlenbeck process \(X = X(\theta, \sigma)\), starting at \(X_0=x_0\), is a centered GP with covariance function

A Brownian Bridge \(B= {B_t : t\in [0,1]}\) is a centered GP with covariance function

9.2.3. Counterexamples#

A Geometric Browanian motion is not a Gaussian process as its marginal distributions are log-normal, not Gaussian.

A CIR process is not a Gaussian process as its marginal distributions are scaled Chi-square, not Gaussian.

A Bessel process is not a Gaussian process as its marginal distributions are non-central chi, not Gaussian.

9.3. Simulation#

In order to simulate paths from a Gaussian process \(X \sim \mathcal{GP}(m, k)\), we need to set a discrete partition over an interval for the simulation to take place.

For simplicity, we are going to consider an equidistant partition of size \(n\) over \([0,T]\), i.e.:

By definition, the joint distribution of

is multivariate Gaussian. Therefore, we can get a path by sampling from a multivariate normal distribution with mean vector \(\mu = [m(t_1), \cdots, m(t_n)]\) and covariance matrix

To do this, we will use the multivariate_normal function from the numpy.random module.

As an example let’s simulate paths from a Brownian motion. First, we construct the partition, using np.linspace, and define the covariance function.

import numpy as np

T = 1.0 # End point of the interval to simulate [O,T]

n = 100 # Number of points in the partition

times = np.linspace(0, T, n) # Partition

# Covariance Function (Kernel) for Brownian Motion

def brownian_cov(t):

return np.minimum.outer(t, t)

Then, we simply sample from the multivariate normal distribution with mean vector of zeros and covariance matrix given by the Brownian motion covariance function.

from numpy.random import multivariate_normal

N = 5 # Number of sample paths to simulate

samples = multivariate_normal(mean=np.zeros(n), cov=brownian_cov(times), size=N)

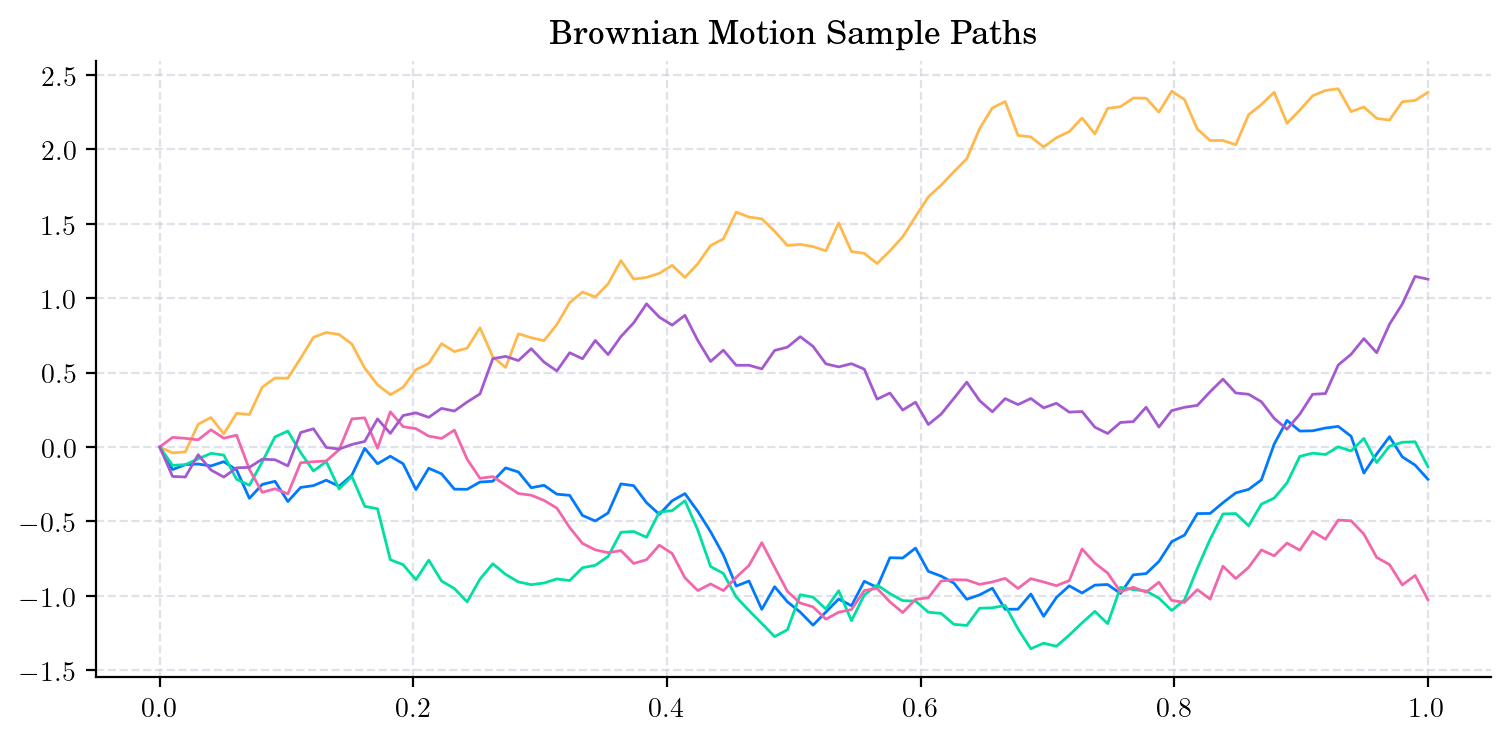

Finally, we plot the simulated paths

for sample in samples:

plt.plot(times, sample, "-", lw=1)

plt.title("Brownian Motion Sample Paths")

plt.show()

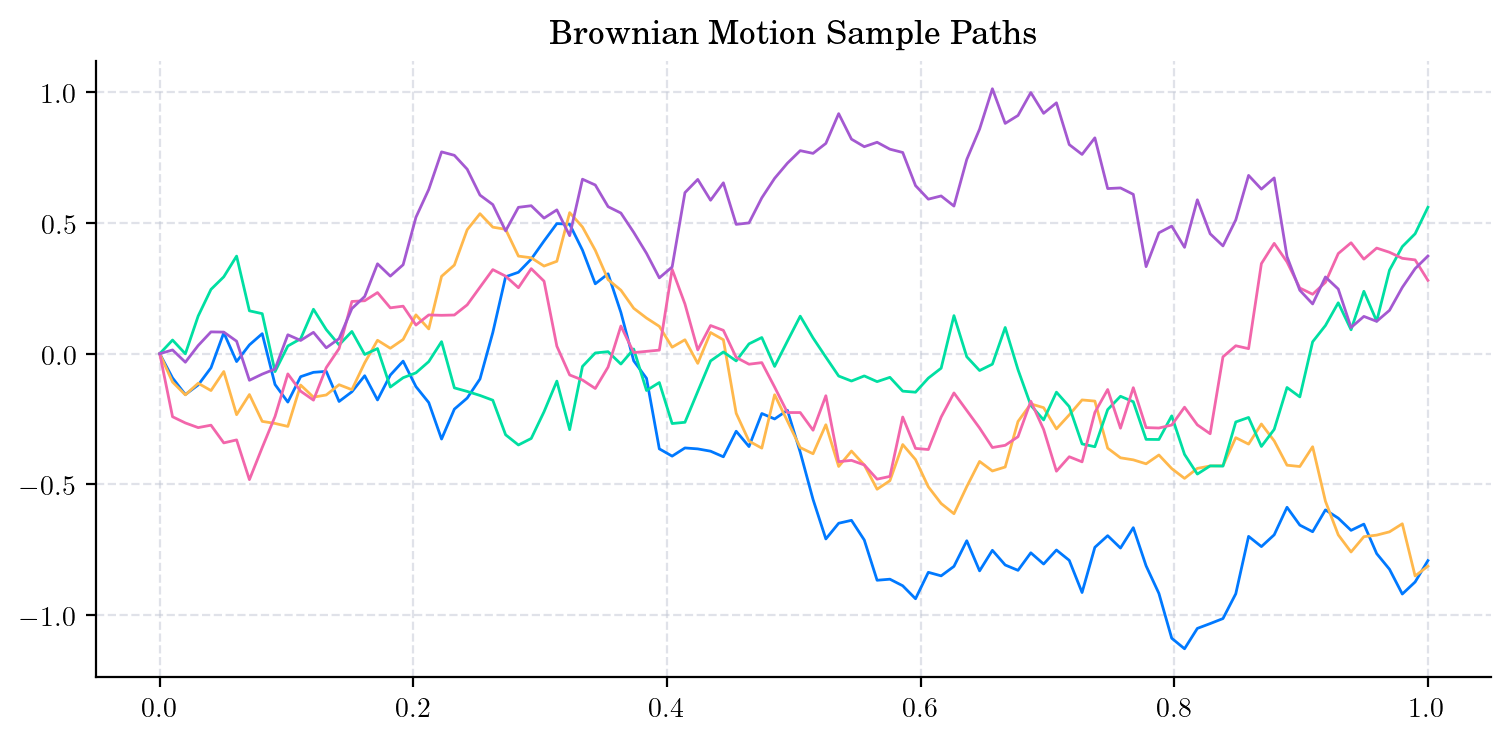

Putting these steps together we get the following snippet

# Snippet to generate multiple sample paths from a Gaussian Process (Brownian Motion) and plot them

import numpy as np

from numpy.random import multivariate_normal

import matplotlib.pyplot as plt

T = 1.0 # End point of the interval to simulate [O,T]

n = 100 # Number of points in the partition

times = np.linspace(0, T, n) # Partition

# Covariance Function (Kernel) for Brownian Motion

def covariance_function(t):

return np.minimum.outer(t, t)

N = 5 # Number of sample paths to generate

samples = multivariate_normal(mean=np.zeros(n), cov=covariance_function(times), size=N) # Sample paths

for sample in samples:

plt.plot(times, sample, "-", lw=1)

plt.title("Brownian Motion Sample Paths")

plt.show()

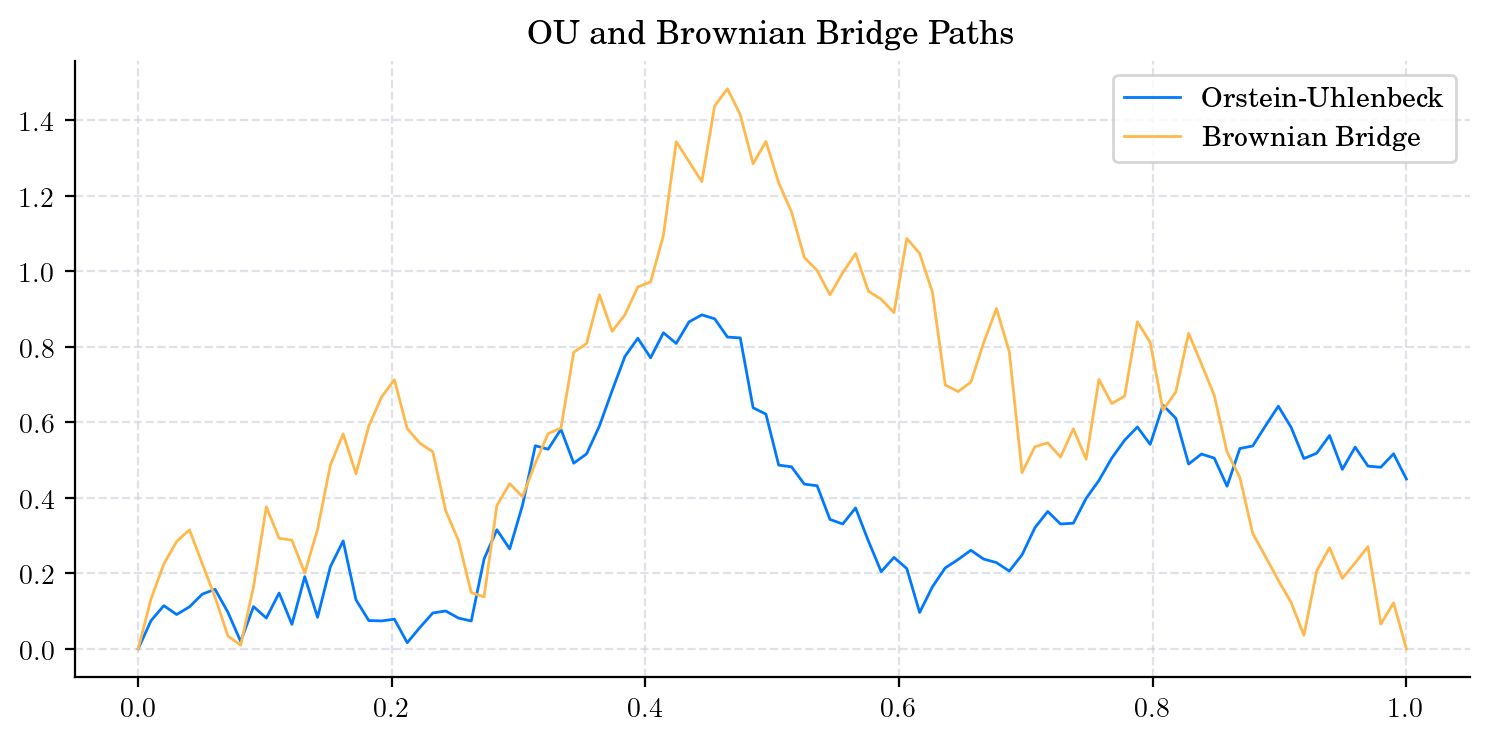

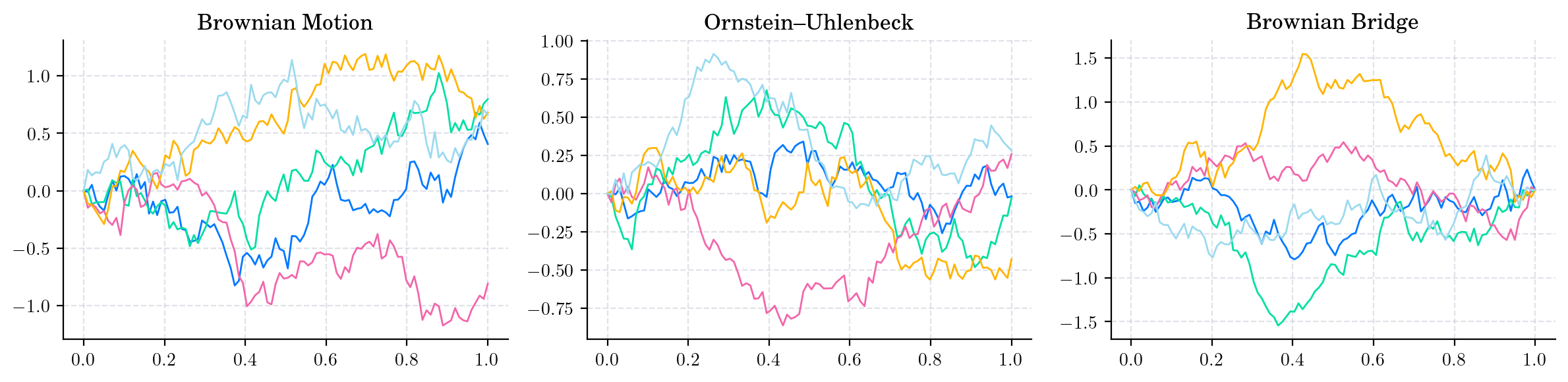

Similarly, we can simulate paths from an Orstein-Uhlenbeck process and a Brownian Bridge.

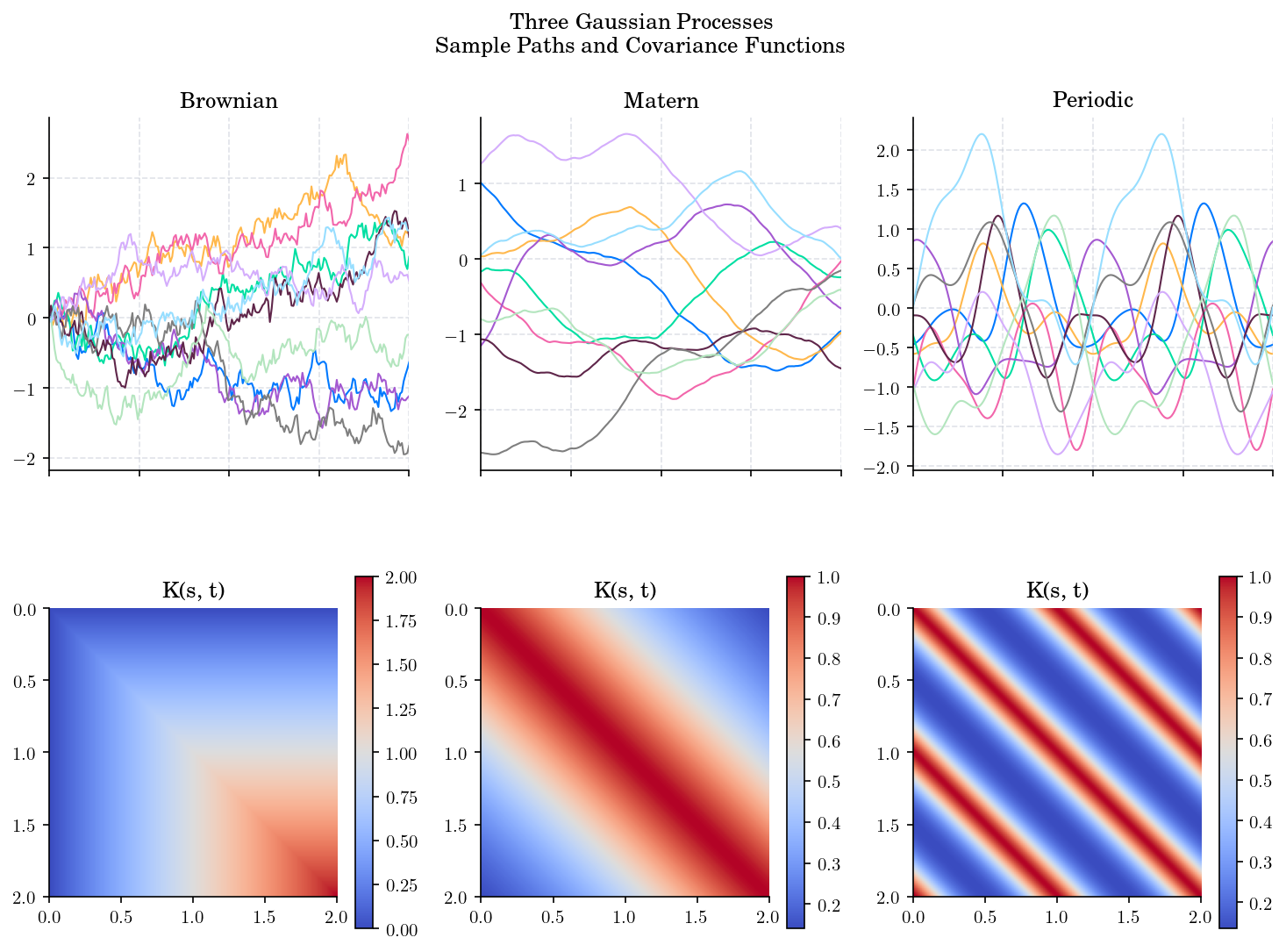

The following plot shows the simulated paths from a Brownian motion, an Orstein-Uhlenbeck process and a Brownian Bridge. It illustrates the different behaviours of these processes, which are all Gaussian processes but with different covariance structures.

9.4. Covariance Functions/Kernels#

In practice, the mean function is often taken to be zero (since any process can be centered), so the covariance function (kernel) fully characterizes the behaviour of the process.

Let \( X = {X(t) : t \in \mathcal{T}} \) be a stochastic process. Its covariance function is given by

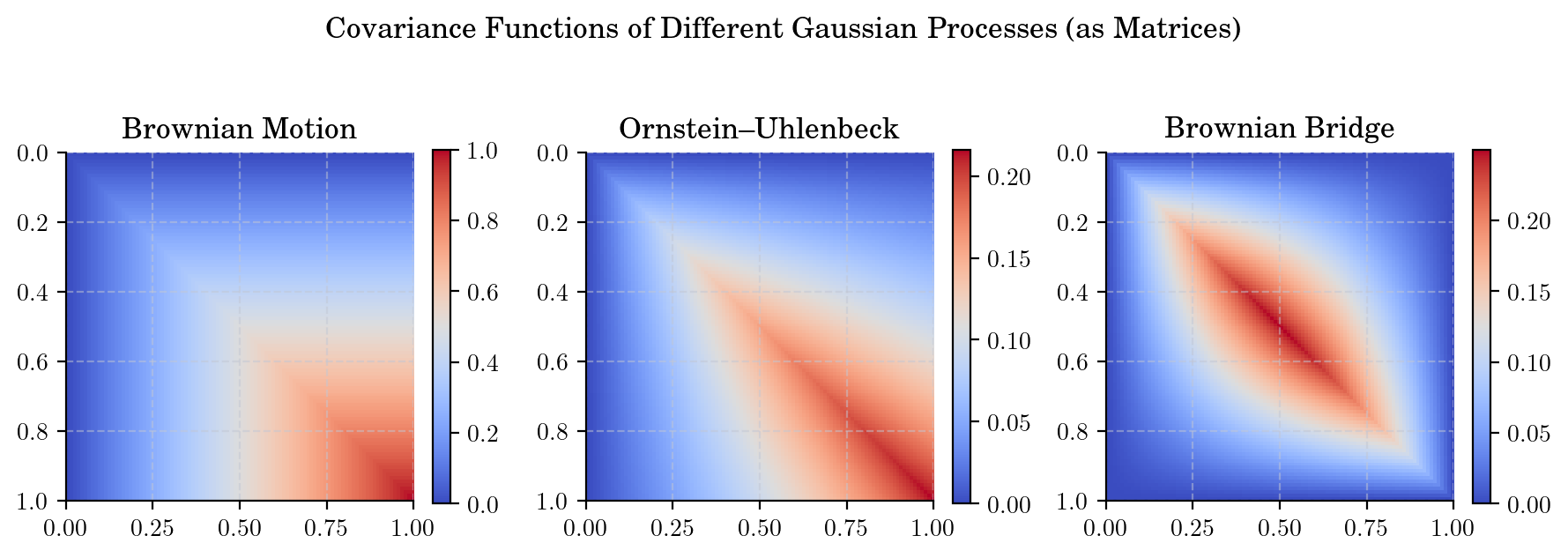

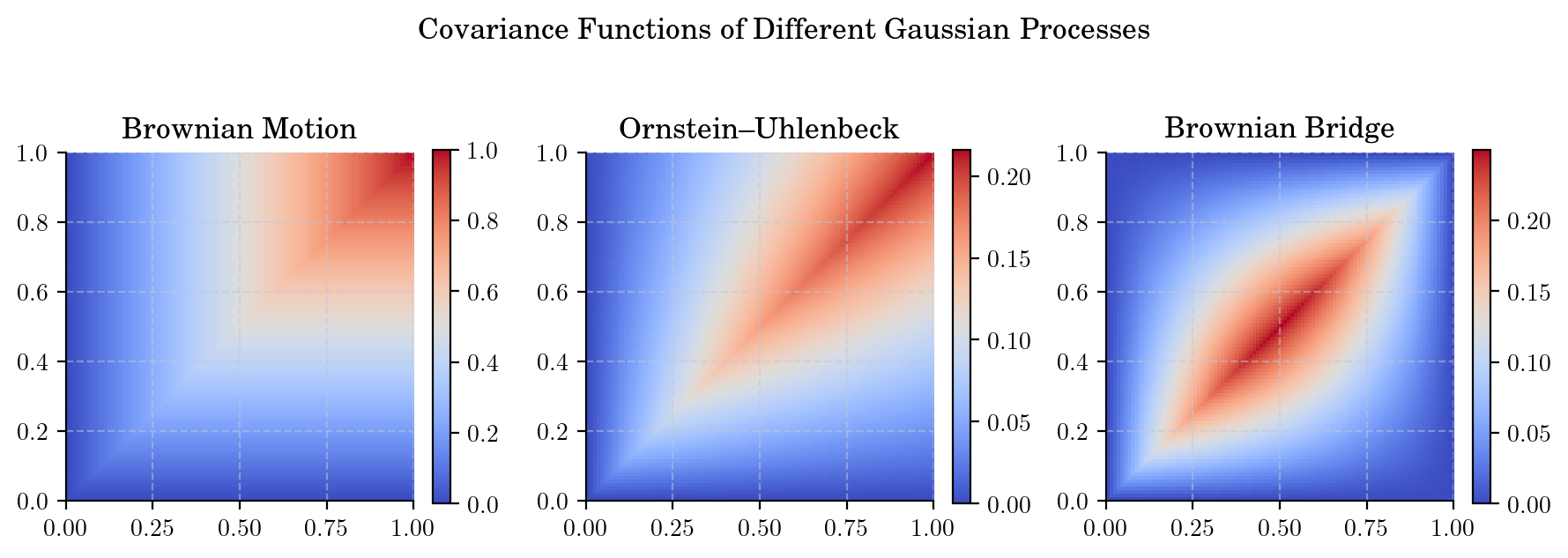

One can visualize this function in two ways:

as a matrix, where the \((i,j)\)-th entry is \(k(t_i, t_j)\) for a given partition \(\{t_1, \cdots, t_n\}\) of the interval \([0,T]\)

as a function of two variables, where the value of the function at \((s,t)\) is \(k(s,t)\).

Let’s visualize the covariance functions of the three processes we have simulated above, first as matrices

and then as functions of two variables

Next, let’s put together the paths and covariance functions in a single visualization.

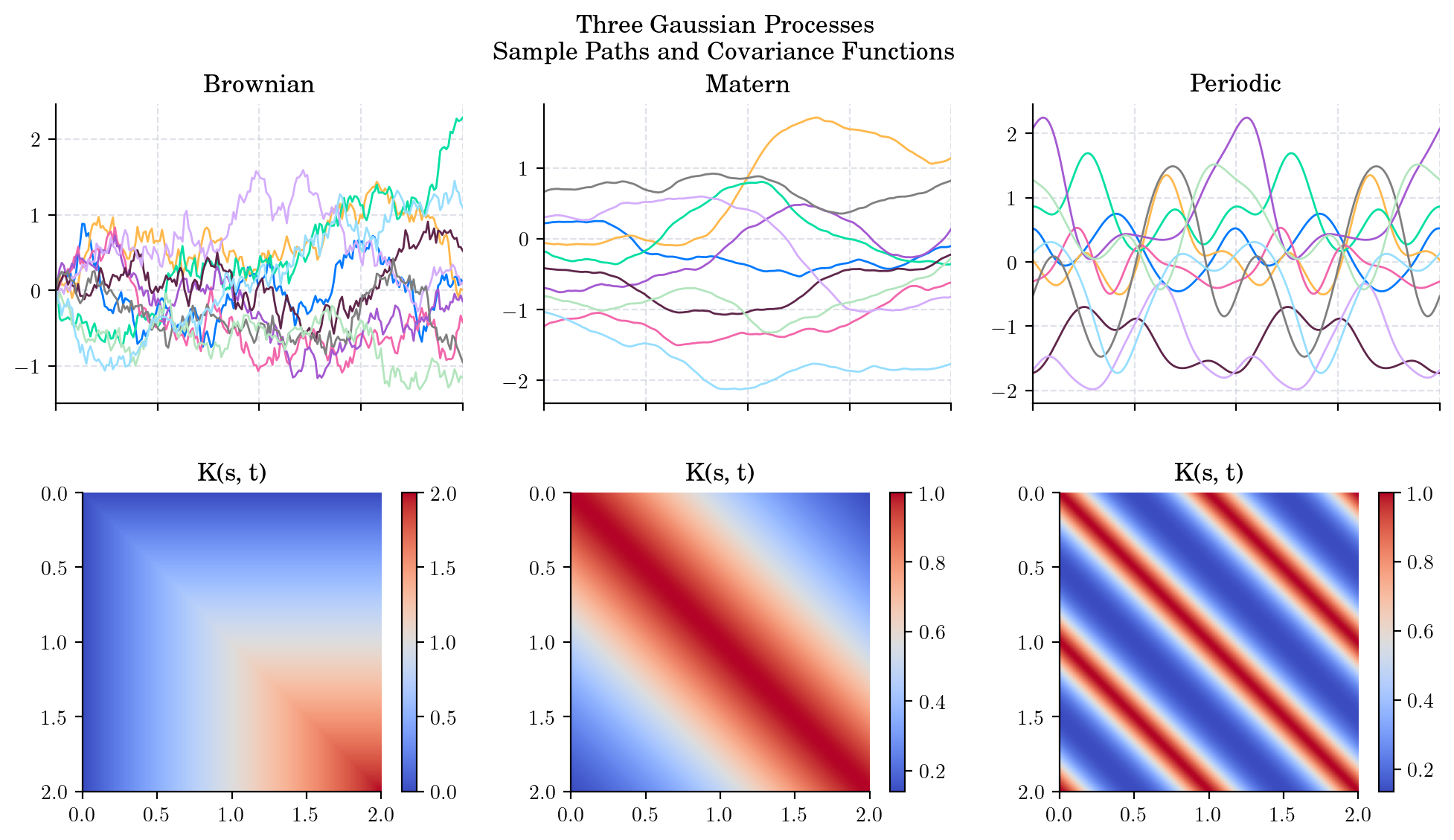

We can visualize other Gaussian processes in a similar way. To do this, we can use the kernel functions provided by the aleatory library.

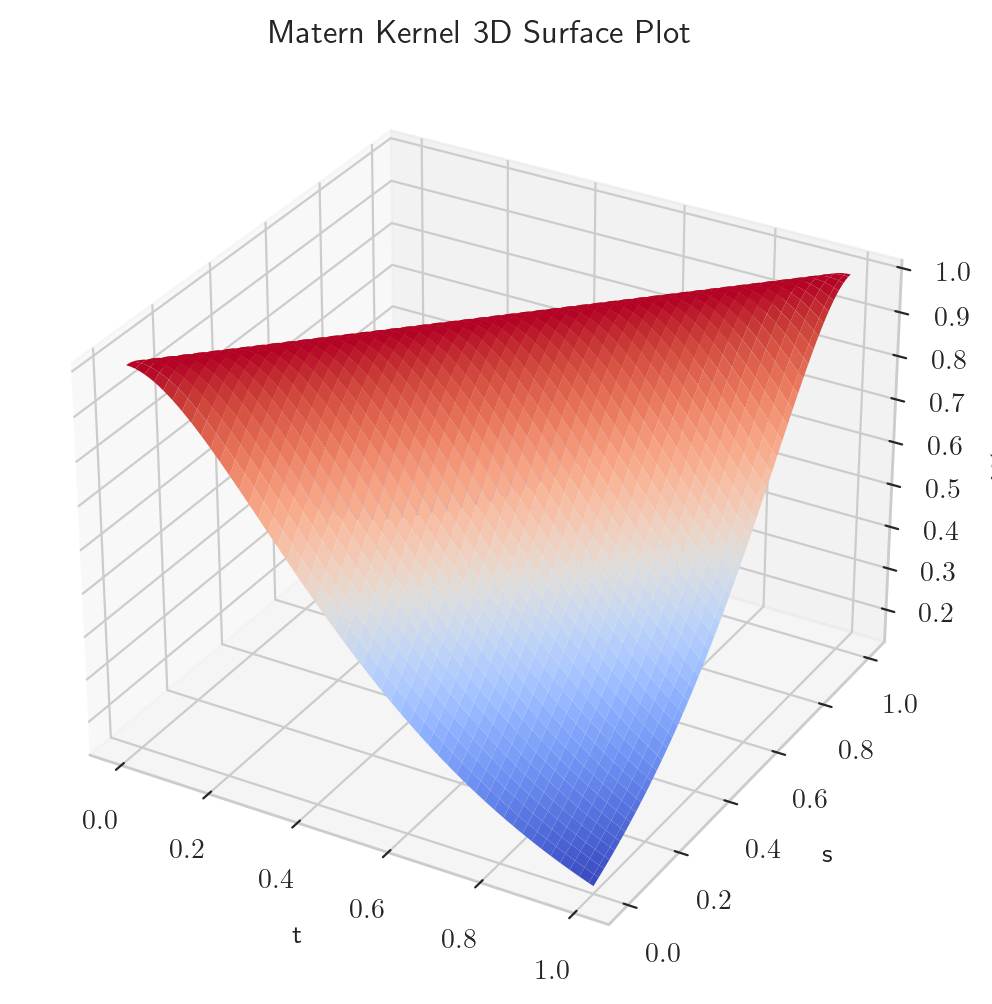

Last but not least, we can visualize the covariance functions using a 3D surface plot, where the x and y axes represent the time points and the z axis represents the covariance values.

9.5. Common Covariance Functions and their corresponding Gaussian Processes#

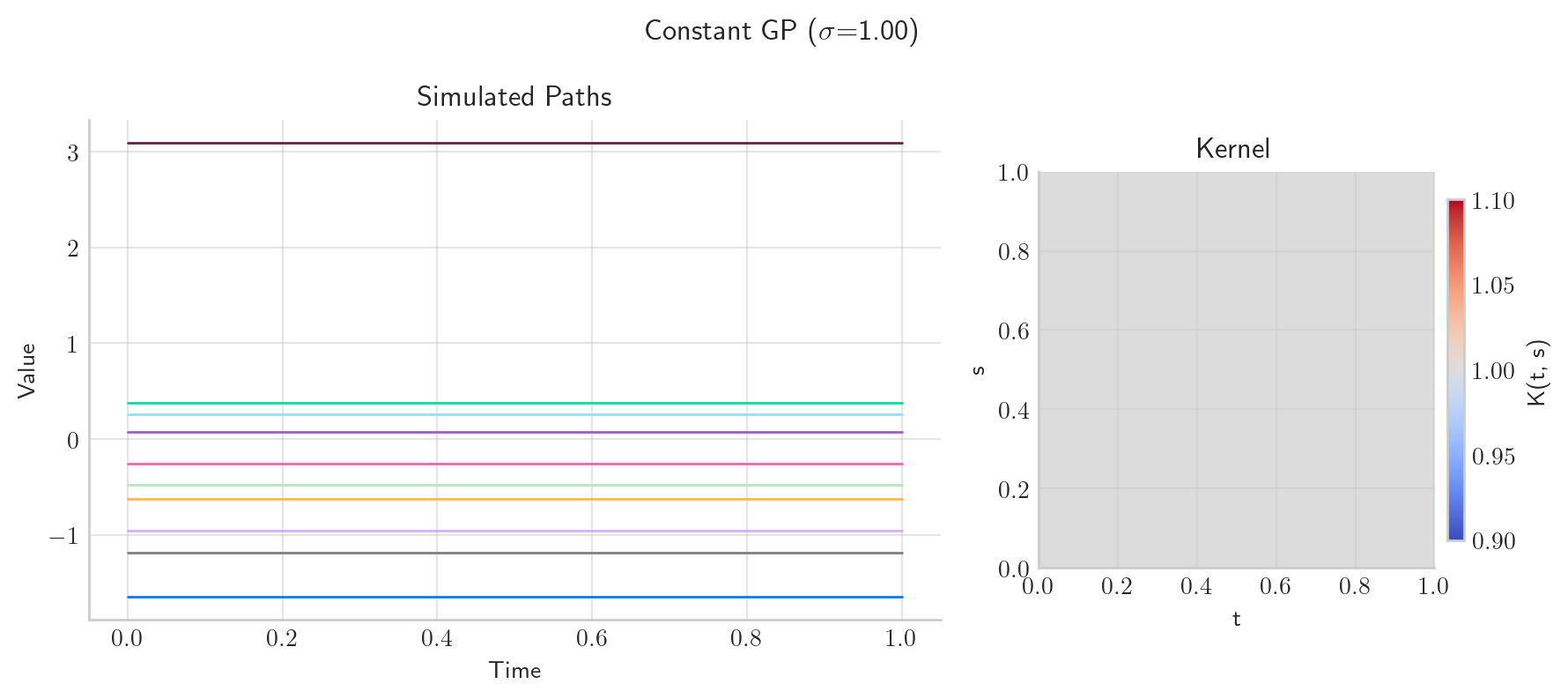

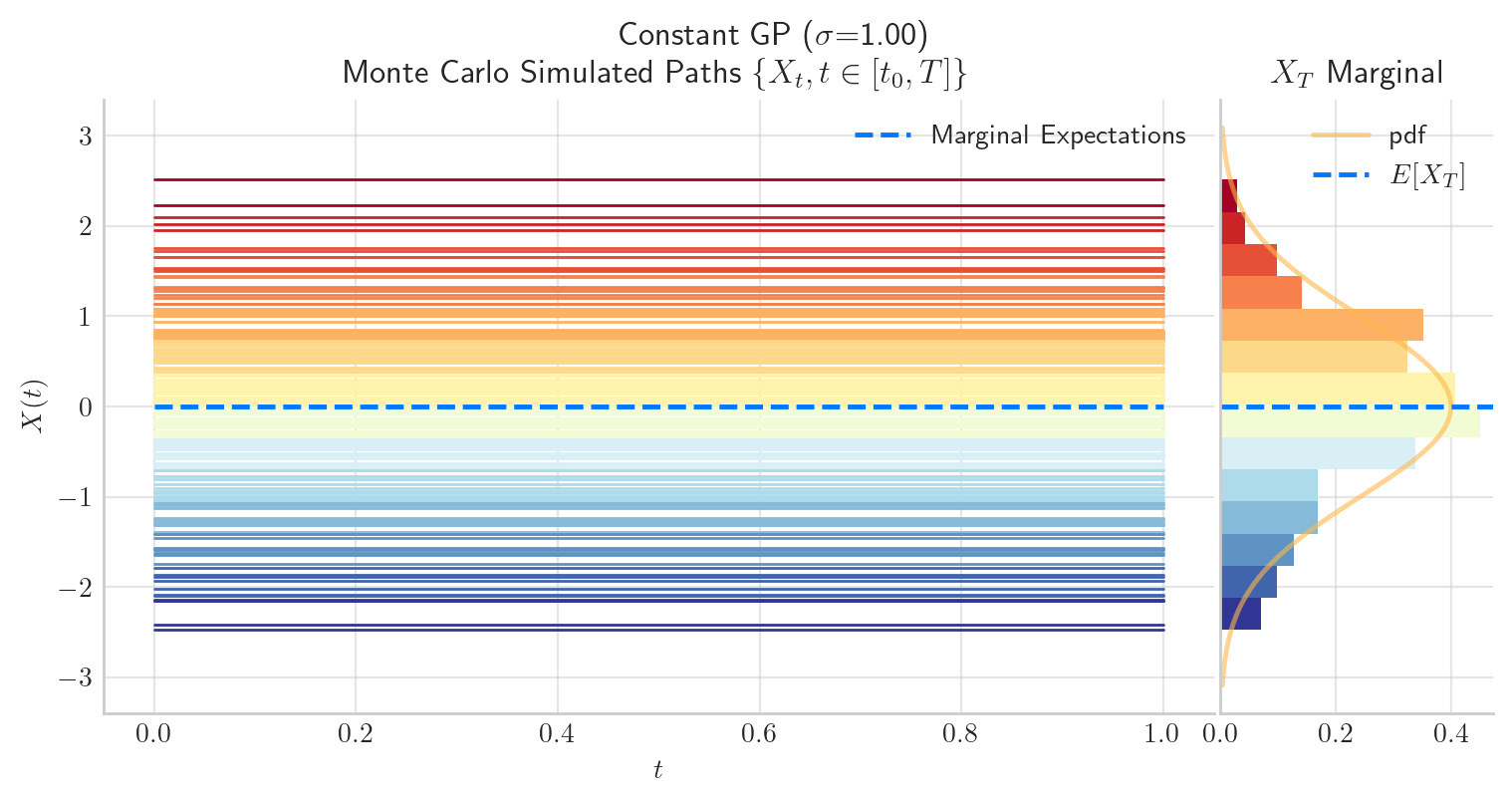

9.5.1. 1. Constant Kernel#

Intuition

All points are perfectly correlated

No dependence on distance

Typical path behaviour

Functions are constant but random in level

Interpretation

The paths are flat but uncertain in magnitude.

from aleatory.processes import GPConstant

p = GPConstant(sigma=1.0)

fig = p.plot_paths_and_kernel(n=100, N=10)

fig = p.draw(n=100, N=200)

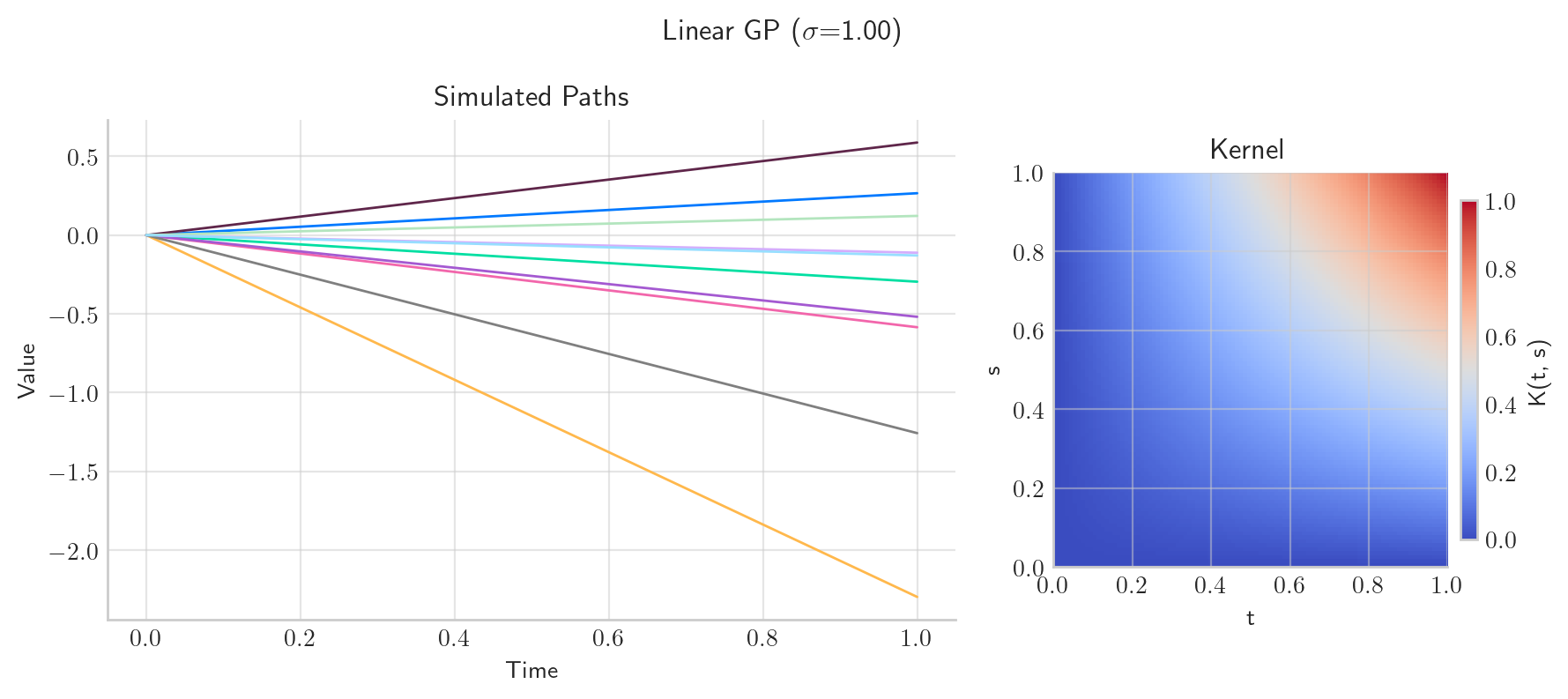

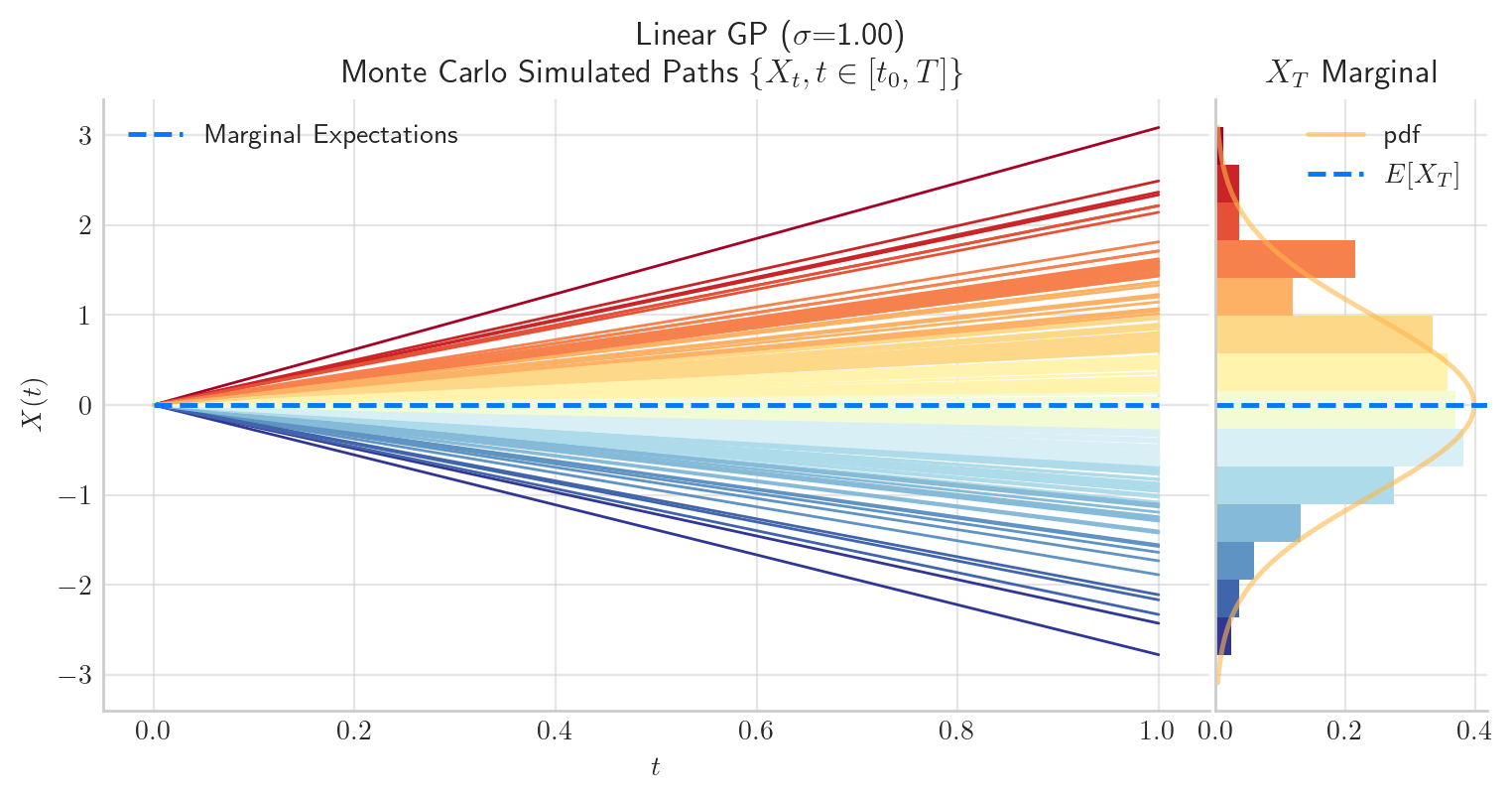

9.5.2. 2. Linear Kernel#

Intuition

Correlation increases with alignment of inputs. Note that the kernel is not stationary, as it depends on the absolute values of the inputs, not just their difference.

Typical paths behaviour

Linear functions

Interpretation

Equivalent to Bayesian linear regression because the kernel is the inner product of the inputs.

from aleatory.processes import GPLinear

p = GPLinear(sigma=1.0, T=1.0)

fig = p.plot_paths_and_kernel(n=100, N=10)

fig = p.draw(n=100, N=200)

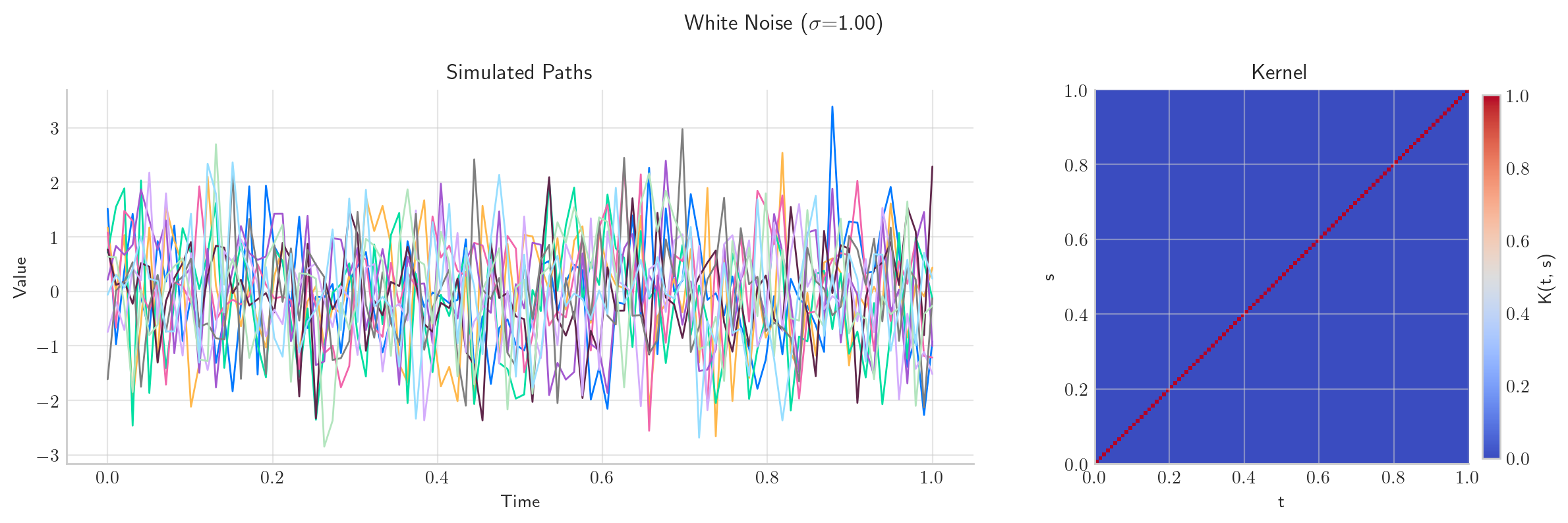

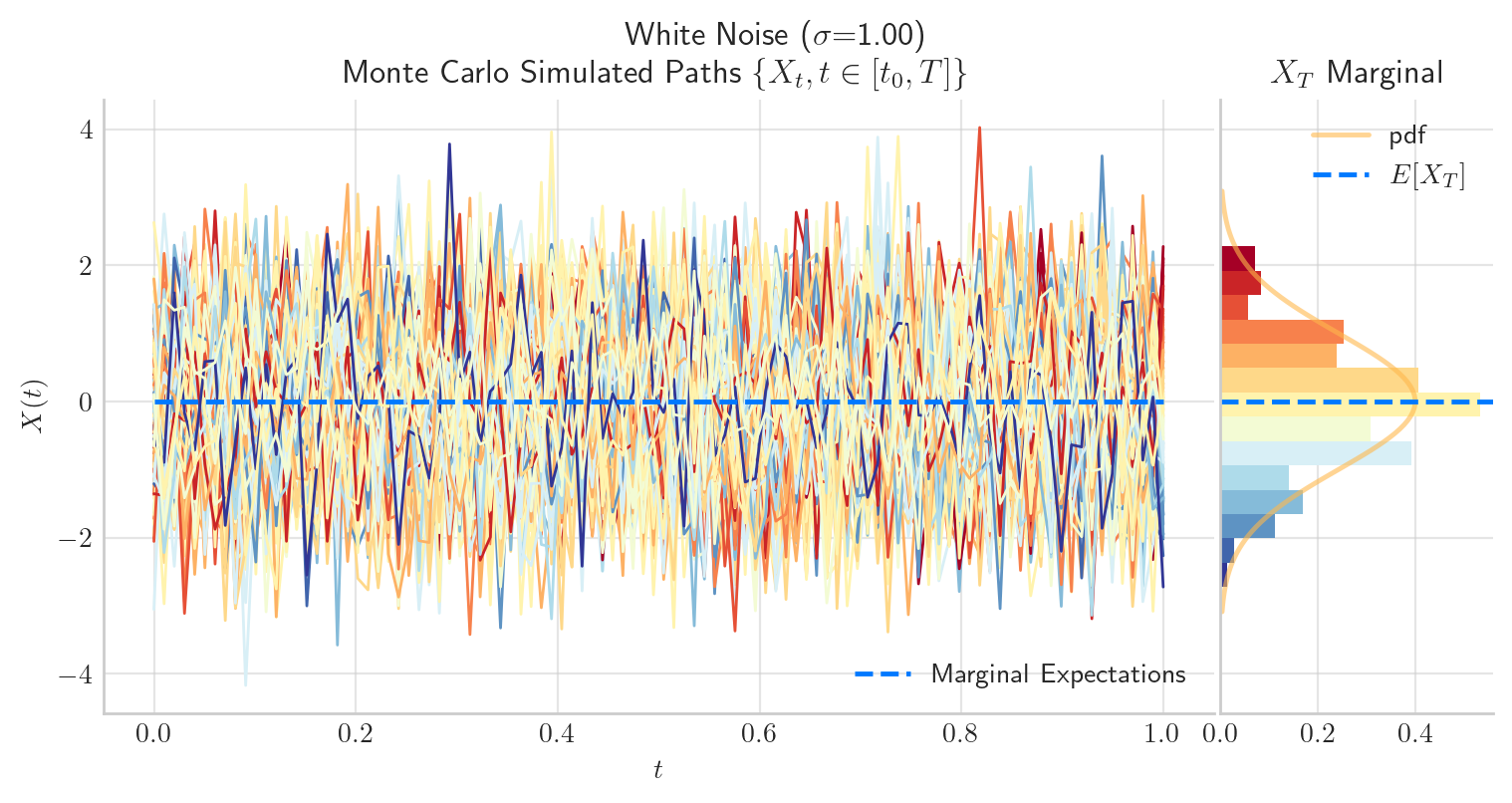

9.5.3. 3. White Noise Kernel#

Intuition

No correlation between different inputs

Typical paths behaviour

Unstructured noise, non-smooth functions

Interpretation

Pure randomness with no smoothness.

from aleatory.processes import WhiteNoise

p = WhiteNoise(sigma=1.0)

fig = p.plot_paths_and_kernel(n=100, N=10, figsize=(12, 4))

fig = p.draw(n=100, N=200, figsize=(9, 4))

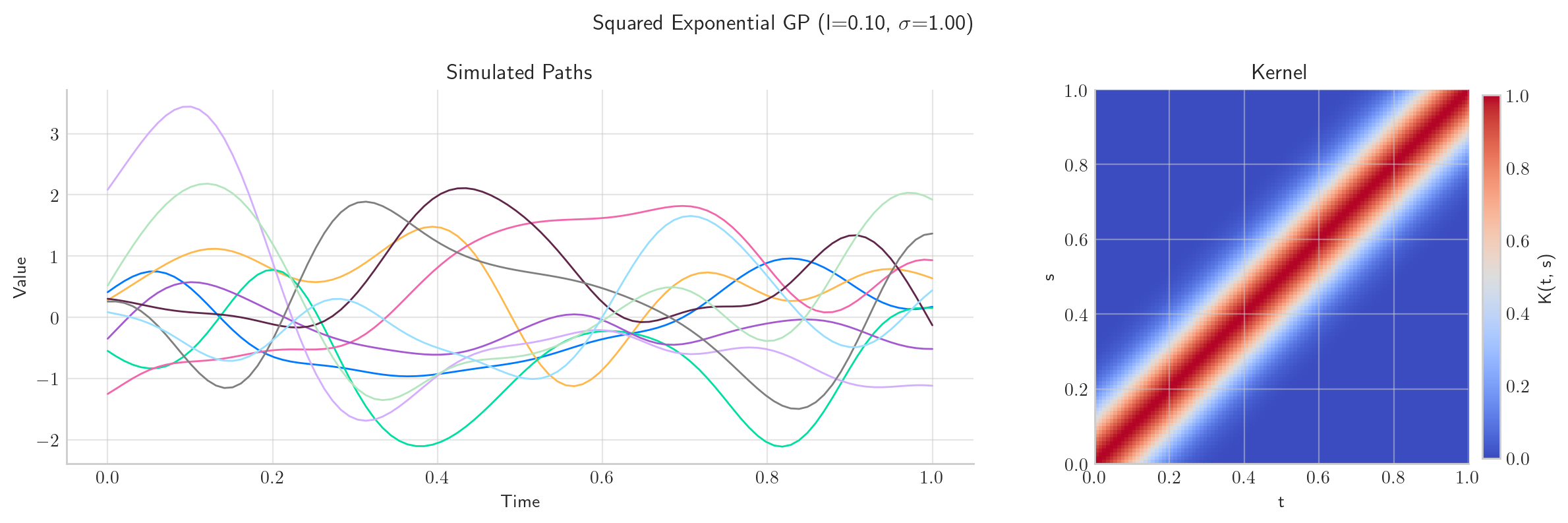

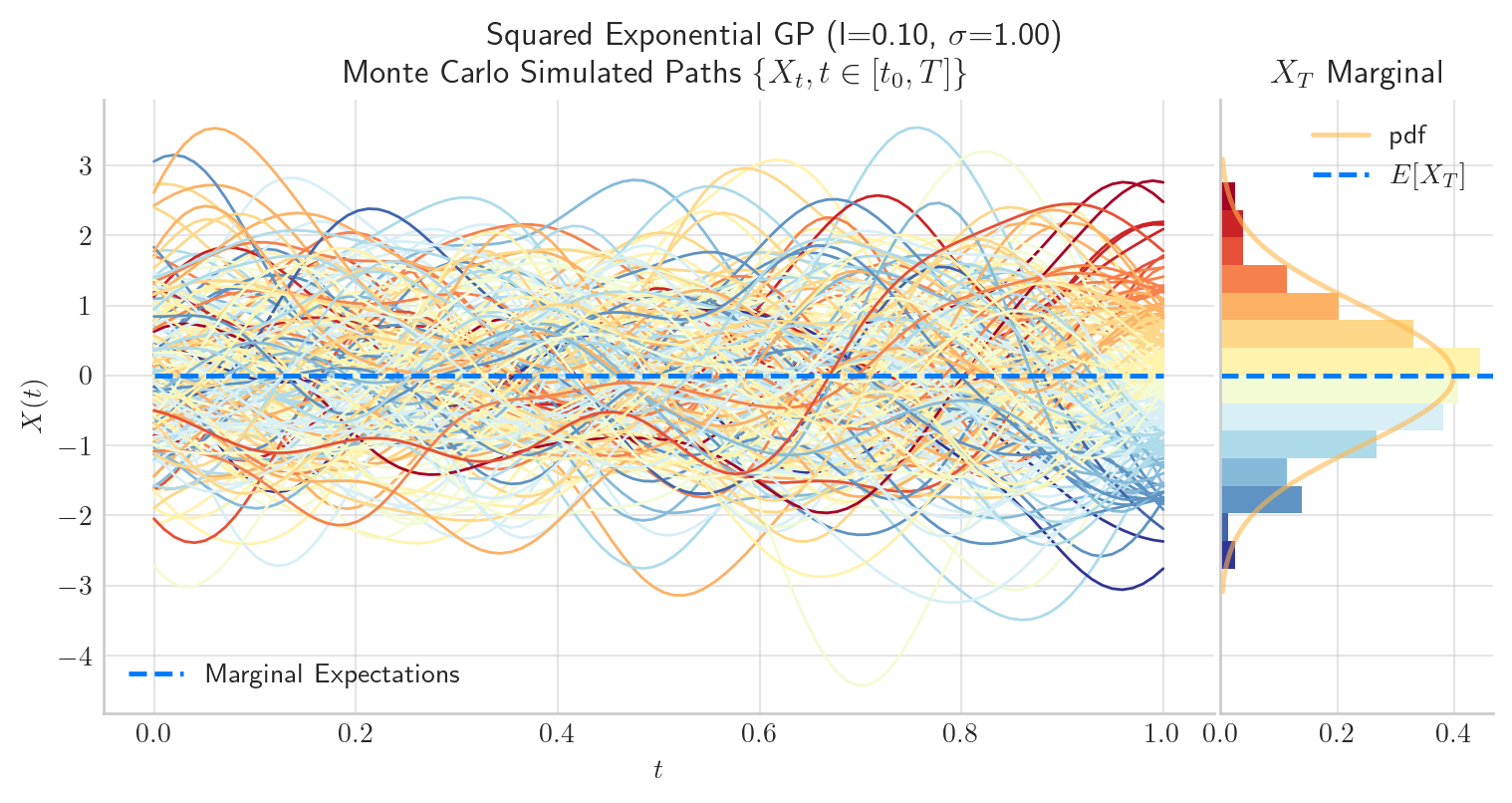

9.5.4. 4. Squared Exponential (RBF) Kernel#

Intuition

Nearby points are strongly correlated

Correlation decays smoothly with distance

Typical paths behaviour

Very smooth functions

Interpretation

Assumes the underlying function is extremely smooth.

from aleatory.processes import GPSquaredExponential

p = GPSquaredExponential(sigma=1.0, length_scale=0.1)

fig = p.plot_paths_and_kernel(n=100, N=10,figsize=(12, 4))

fig = p.draw(n=100, N=200, figsize=(9, 4))

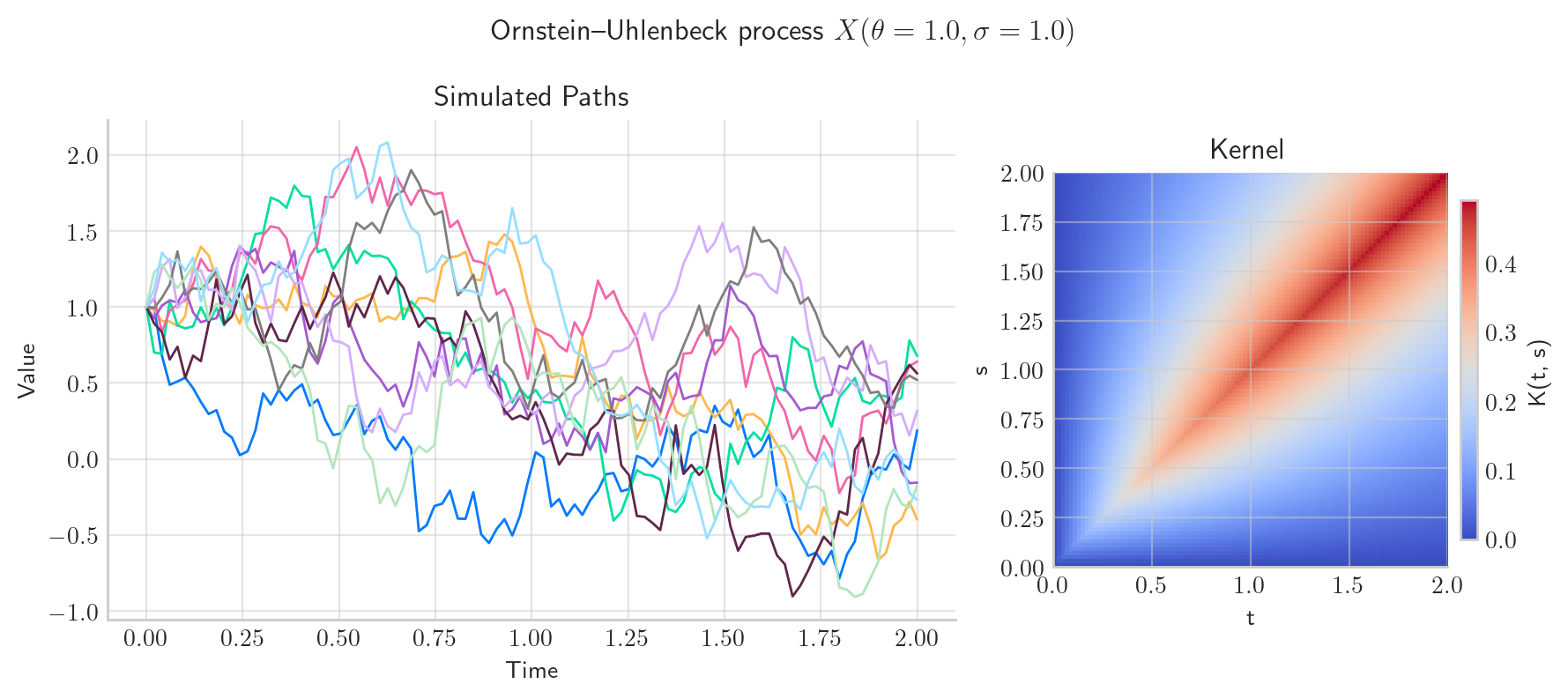

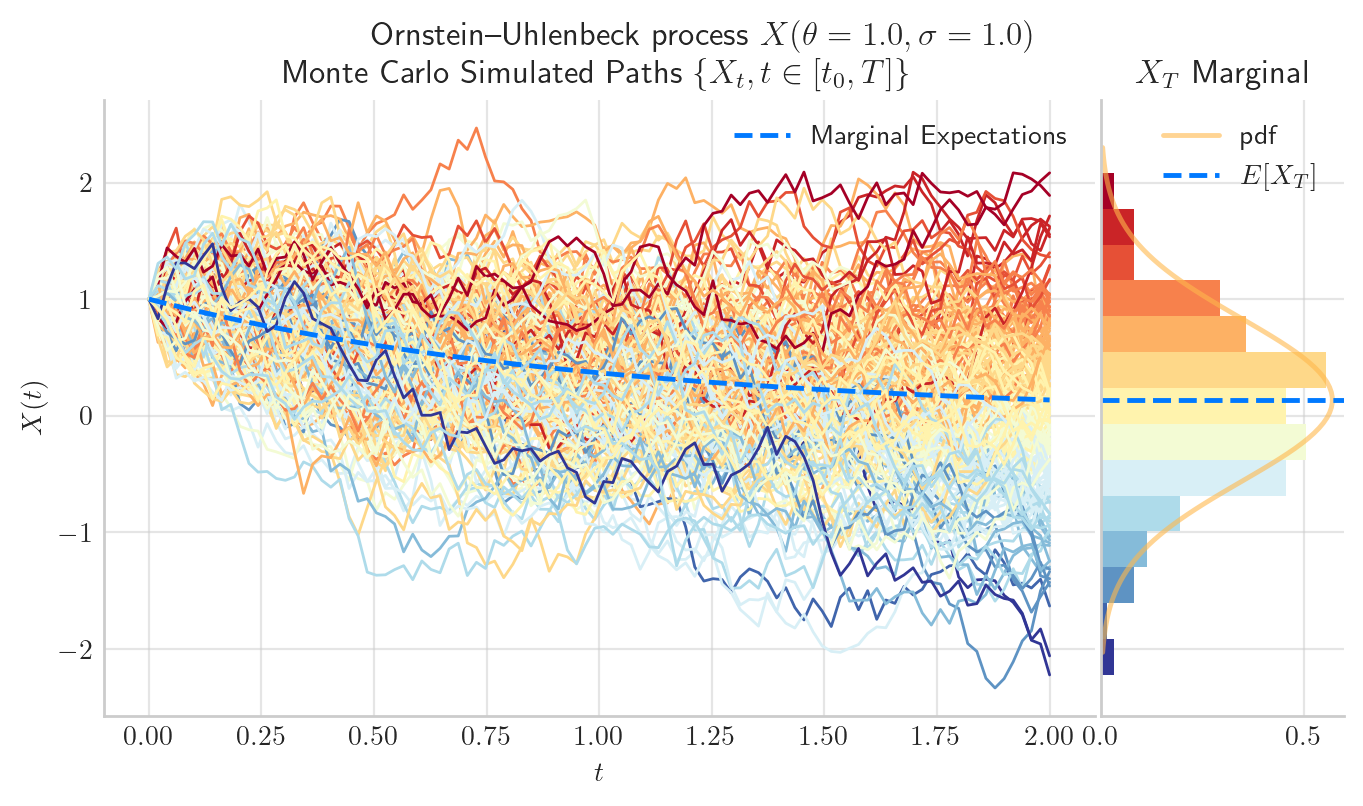

9.5.5. 5. Ornstein–Uhlenbeck Kernel#

Intuition

Correlation decays exponentially with distance

Typical paths behaviour

Continuous but rough paths showing mean-reverting behaviour

Interpretation

Captures mean-reverting behaviour.

from aleatory.processes import OUProcess

p = OUProcess(sigma=1.0, theta=1.0, T=2.0)

fig = p.plot_paths_and_kernel(n=100, N=10)

fig =p.draw(n=100, N=200, figsize=(8, 4))

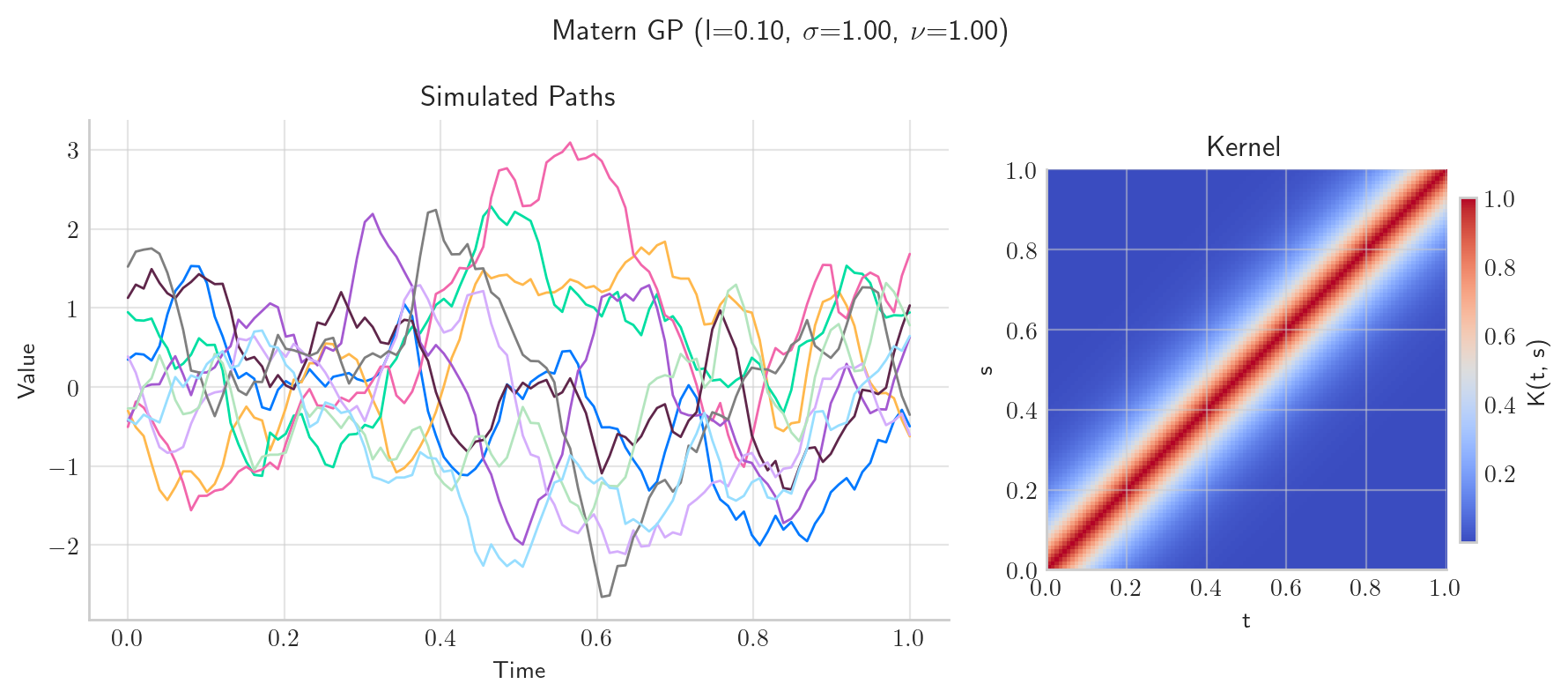

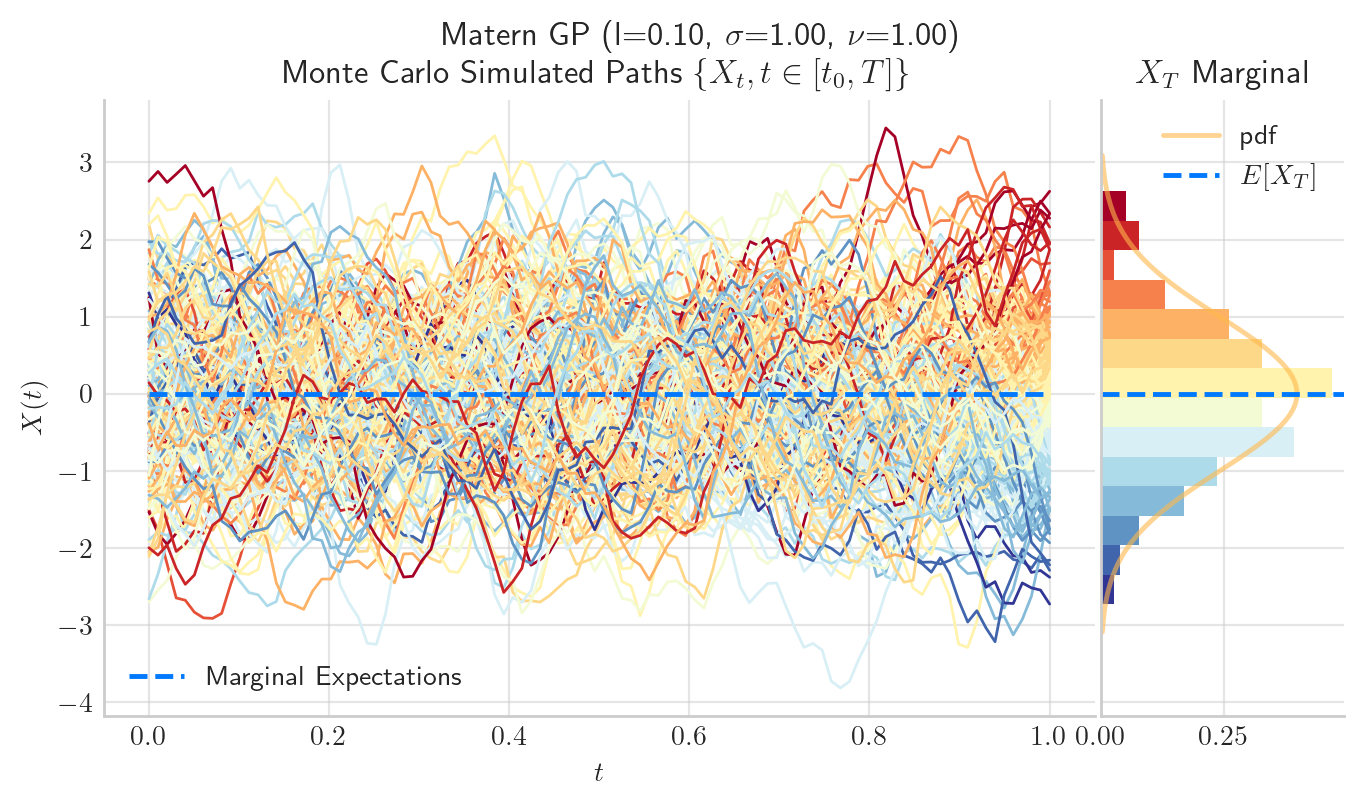

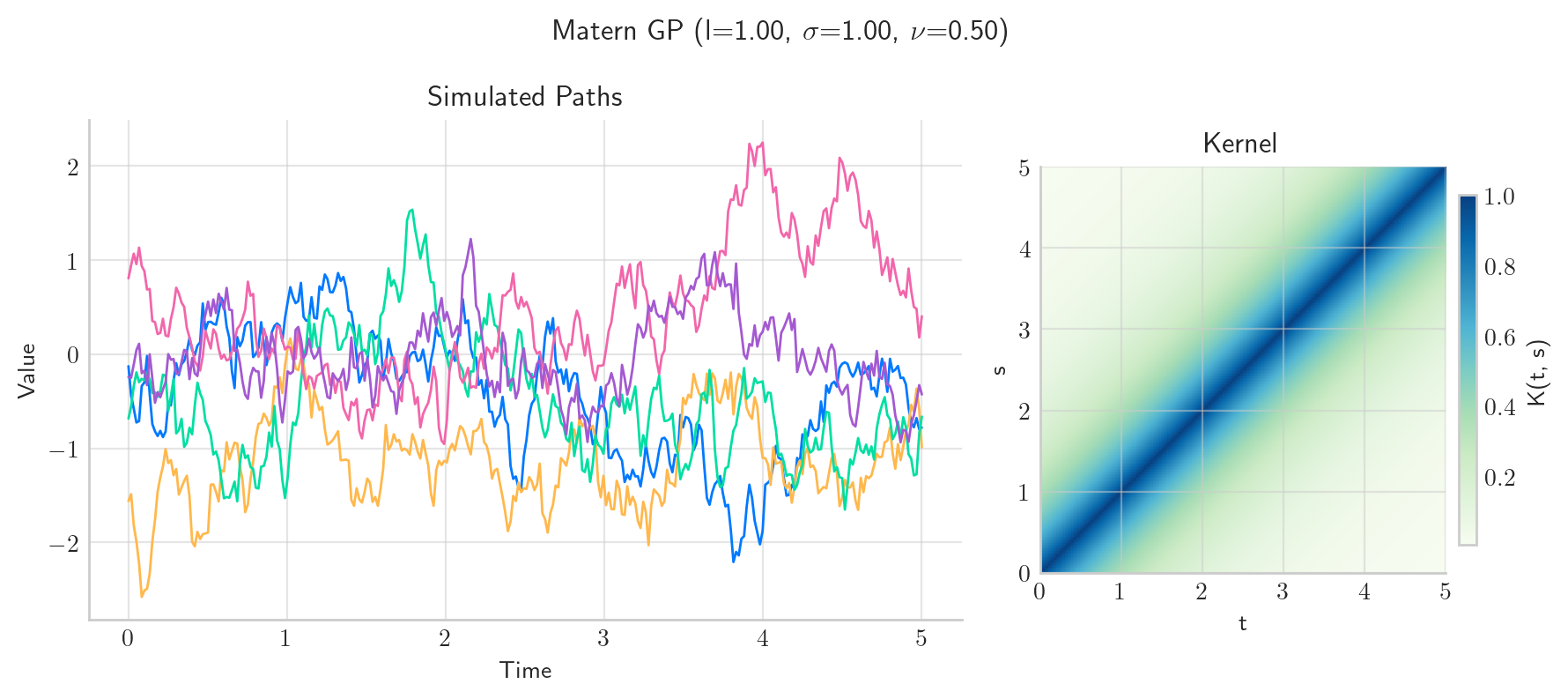

9.5.6. 6. Matérn Kernel#

Intuition

Generalisation of RBF kernel

Smoothness is controlled by the parameter $\( \nu \)$

Special cases

If \( \nu = 1/2 \) → Ornstein–Uhlenbeck kernel

If \( \nu \to \infty \) → Squared exponential kernel

Typical paths behaviour

Tunable smoothness

Interpretation

Provides flexible control over roughness of functions

from aleatory.processes import GPMatern

p = GPMatern(sigma=1.0, length_scale=0.1, nu=1.0)

fig = p.plot_paths_and_kernel(n=100, N=10)

fig = p.draw(n=100, N=200, figsize=(8, 4))

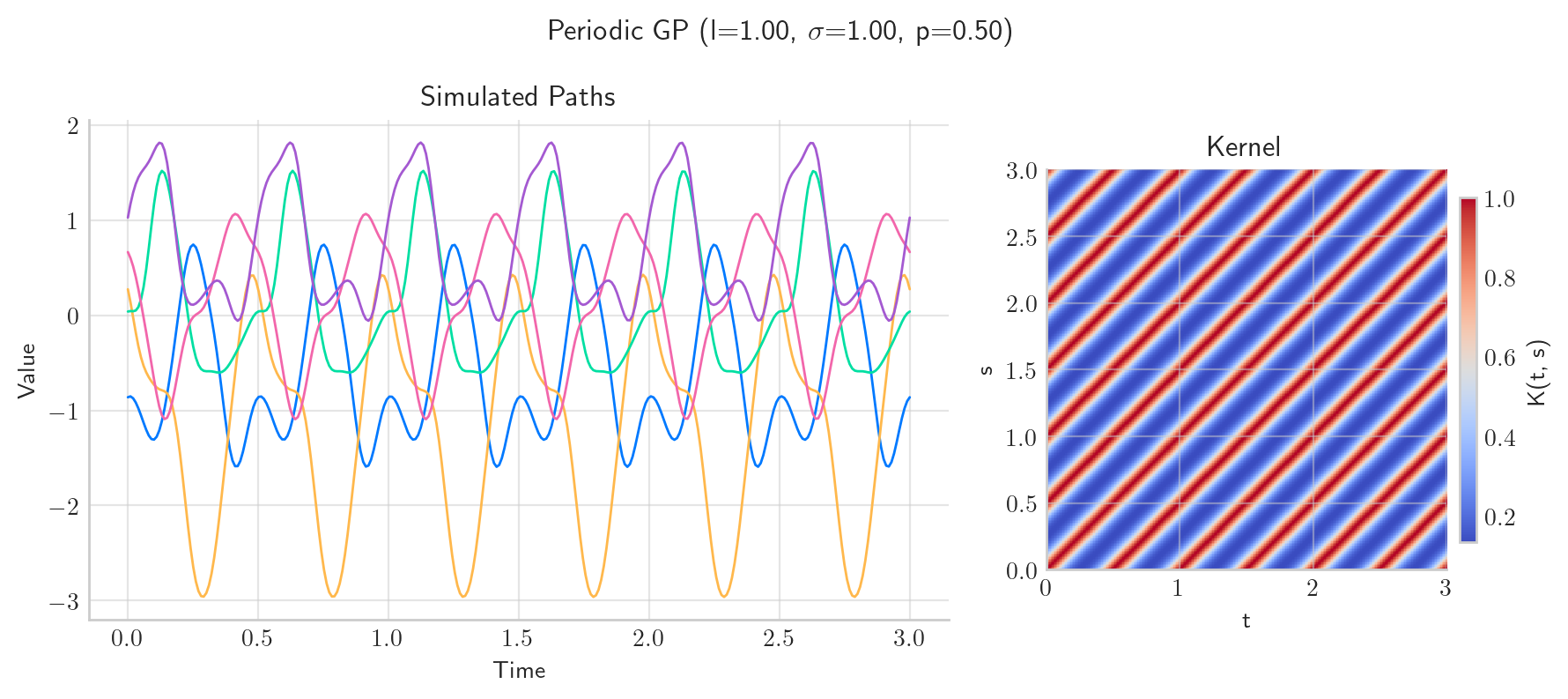

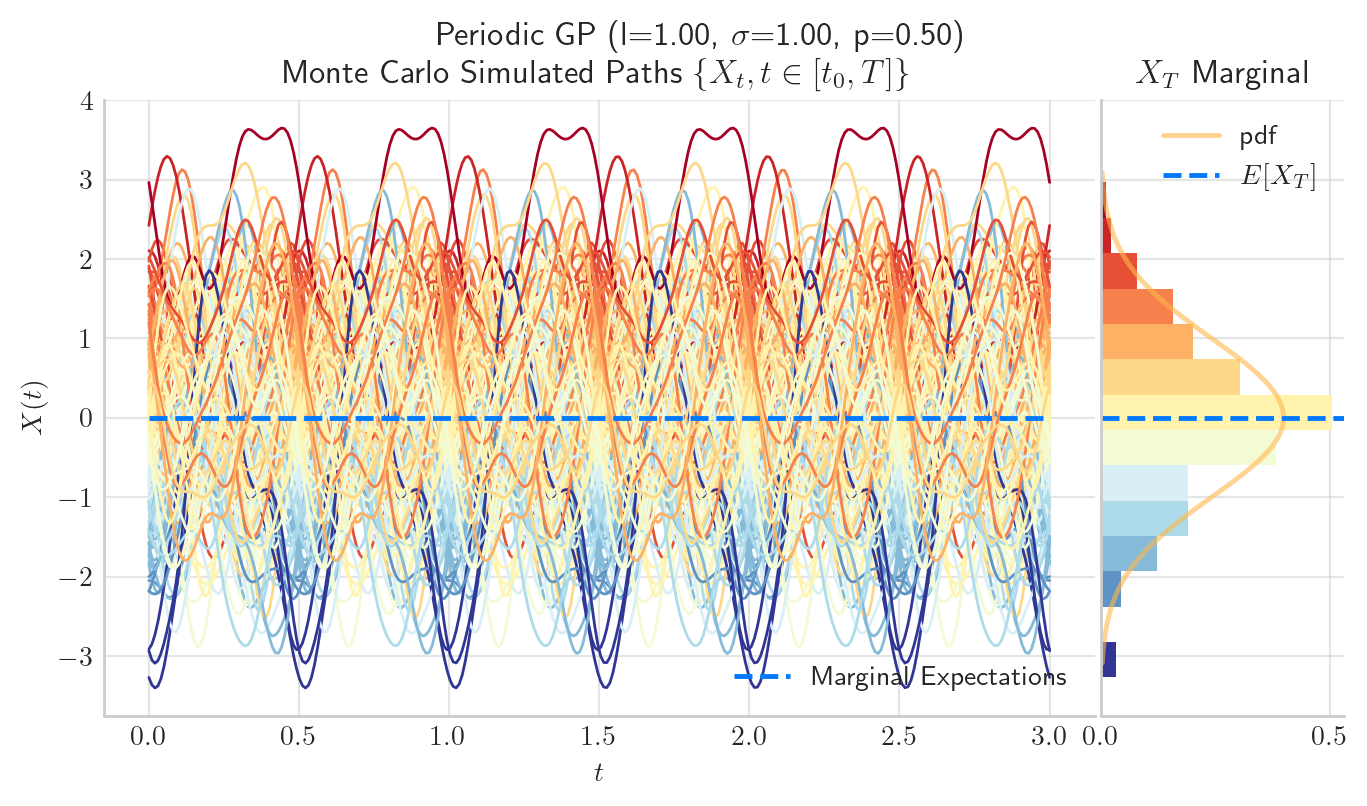

9.5.7. 7. Periodic Kernel#

Intuition

Similarity, repeats periodically

Typical behaviour

Smooth periodic functions

Periodicity is controlled by the parameter \(p\)

Interpretation

Captures seasonality or cyclic behaviour.

from aleatory.processes import GPPeriodic

p = GPPeriodic(T=3.0, sigma=1.0, length_scale=1.0, period=0.5)

fig = p.plot_paths_and_kernel(n=300, N=5)

fig = p.draw(n=300, N=200, figsize=(8, 4))

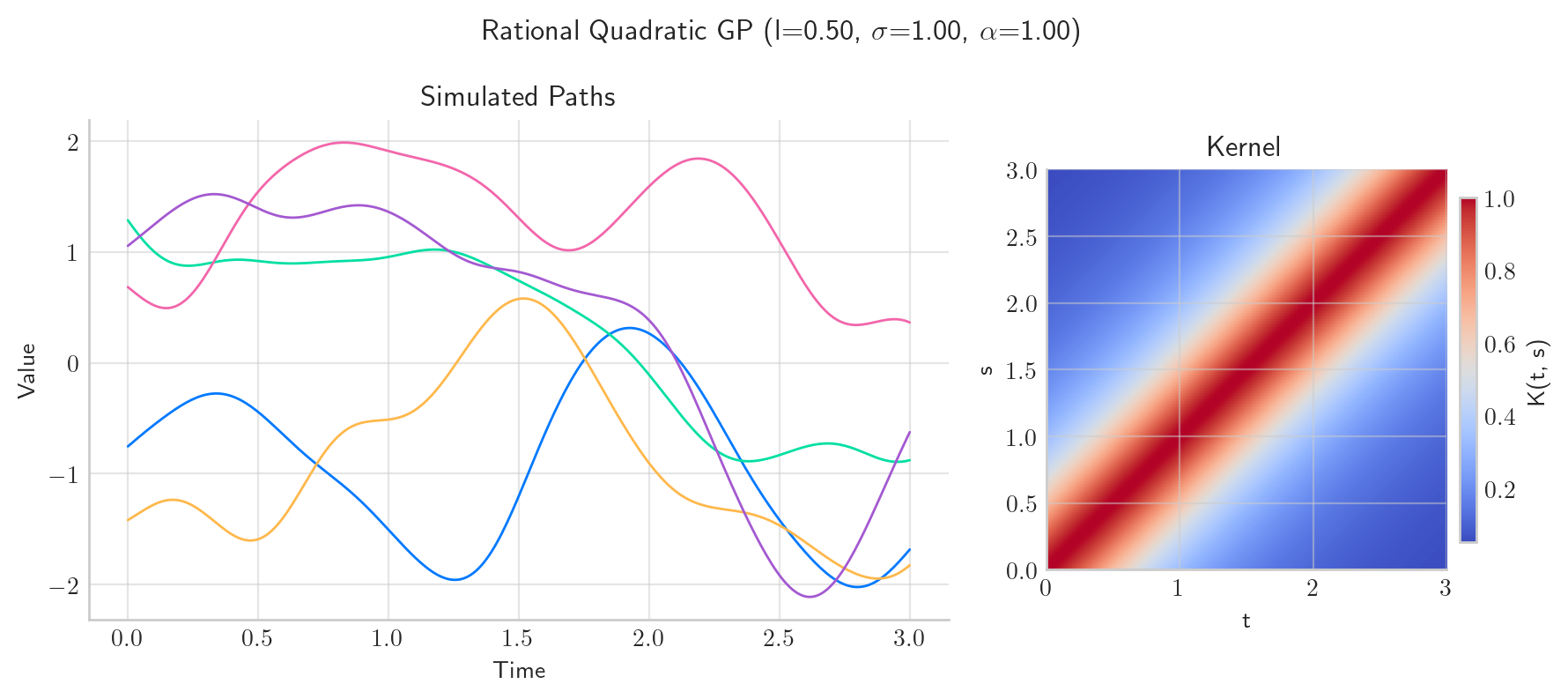

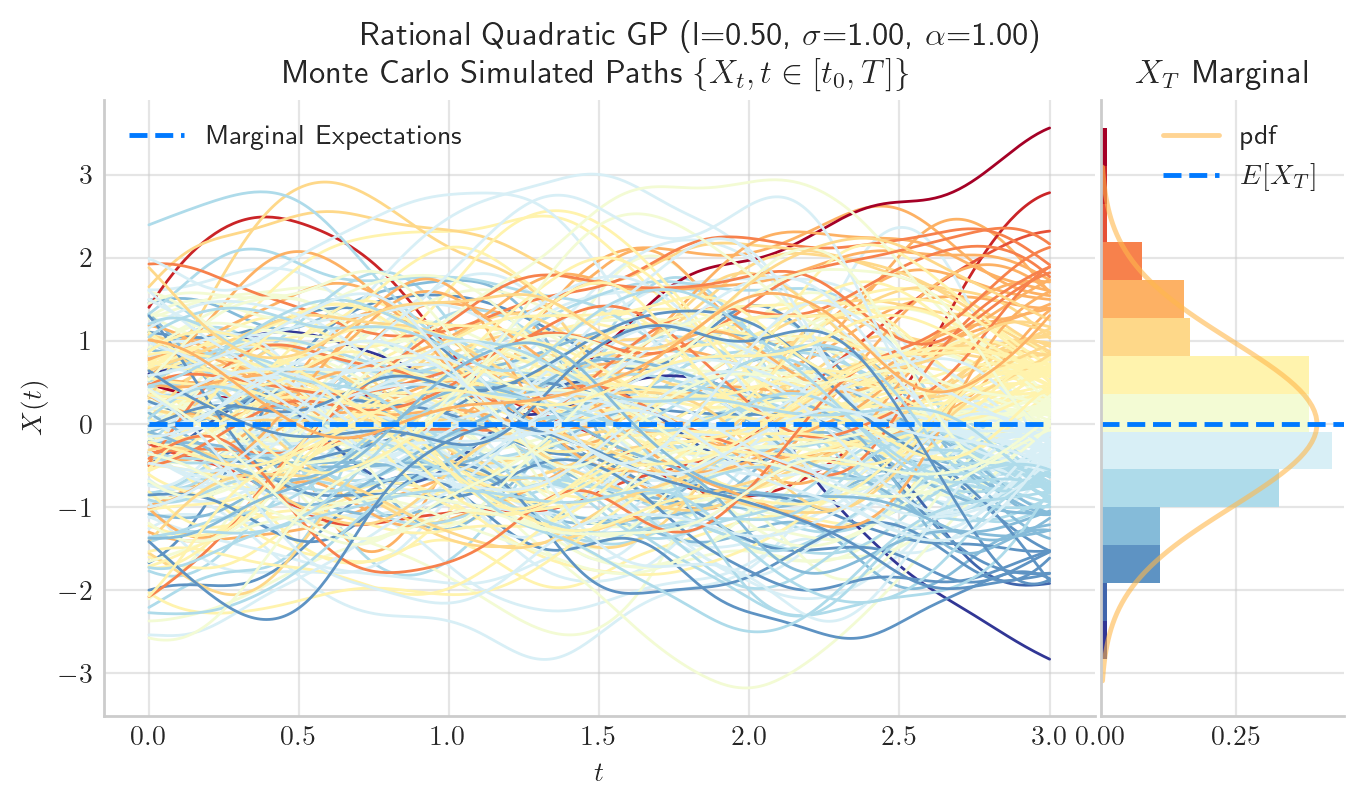

9.5.8. 8. Rational Quadratic Kernel#

Intuition

Mixture of multiple length scales

Typical behaviour

Functions with both short-term and long-term variation

Interpretation

Models multi-scale phenomena.

from aleatory.processes import GPRationalQuadratic

p = GPRationalQuadratic(T=3.0, sigma=1.0, length_scale=0.5, alpha=1.0)

fig = p.plot_paths_and_kernel(n=300, N=5)

fig = p.draw(n=300, N=200, figsize=(8, 4))

9.6. Combining Kernels#

Covariance functions can be combined to model more complex behaviour.

9.6.1. Addition#

Represents the sum of independent effects

9.6.2. Multiplication#

Represents interaction between structures

9.6.3. Example#

Smooth trend + seasonal pattern

9.7. What the Kernel tells us about the Process#

Several structural properties of a Gaussian Proccess \(X\) are encoded in its kernel \(k\), in particular:

9.7.1. Smoothness#

Definition: Smoothness refers to the regularity of sample paths, which can be formalized via mean-square differentiability. A process \(X\) is said to be \(m\)-times mean-square differentiable at \(t\) if the derivatives

exist in \(L^2\) space. This holds if and only if the covariance function \(k(t, s)\) is \(2m\)-times continuously differentiable in a neighbourhood of \(s = t\).

Intuition: The local behaviour of \(k(t,s)\) near the diagonal \(t = s\) determines how rapidly correlations decay between nearby points. If \(k\) is very smooth around the diagonal, nearby values of the process are strongly constrained to vary gradually, leading to smooth sample paths. Conversely, lack of regularity in \(k\) induces rough or highly oscillatory paths.

Examples:

The covariance \(k(t,s) = \min(t,s)\) (Brownian motion) produces paths that are continuous but nowhere differentiable.

The squared exponential (RBF) kernel is infinitely differentiable, hence induces sample paths that are almost surely smooth (indeed, \(C^\infty\)).

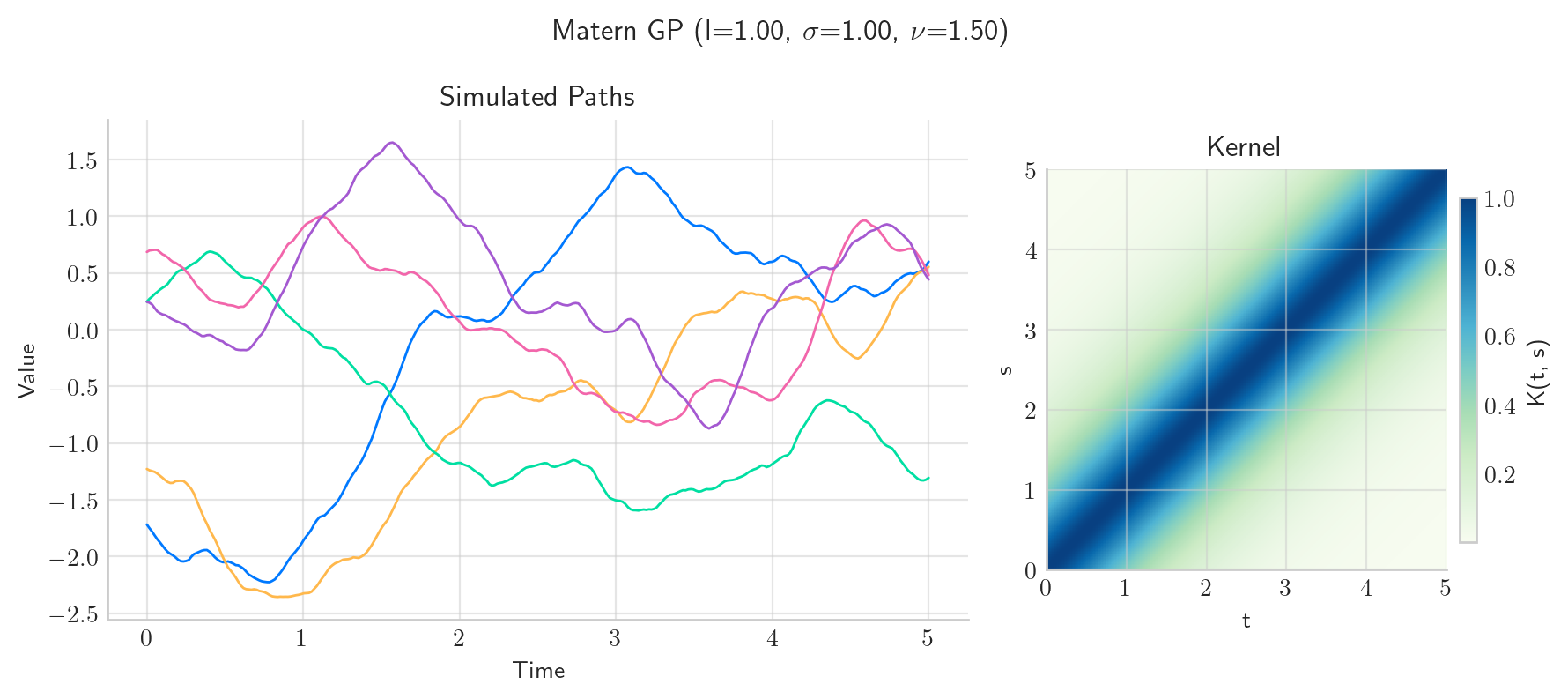

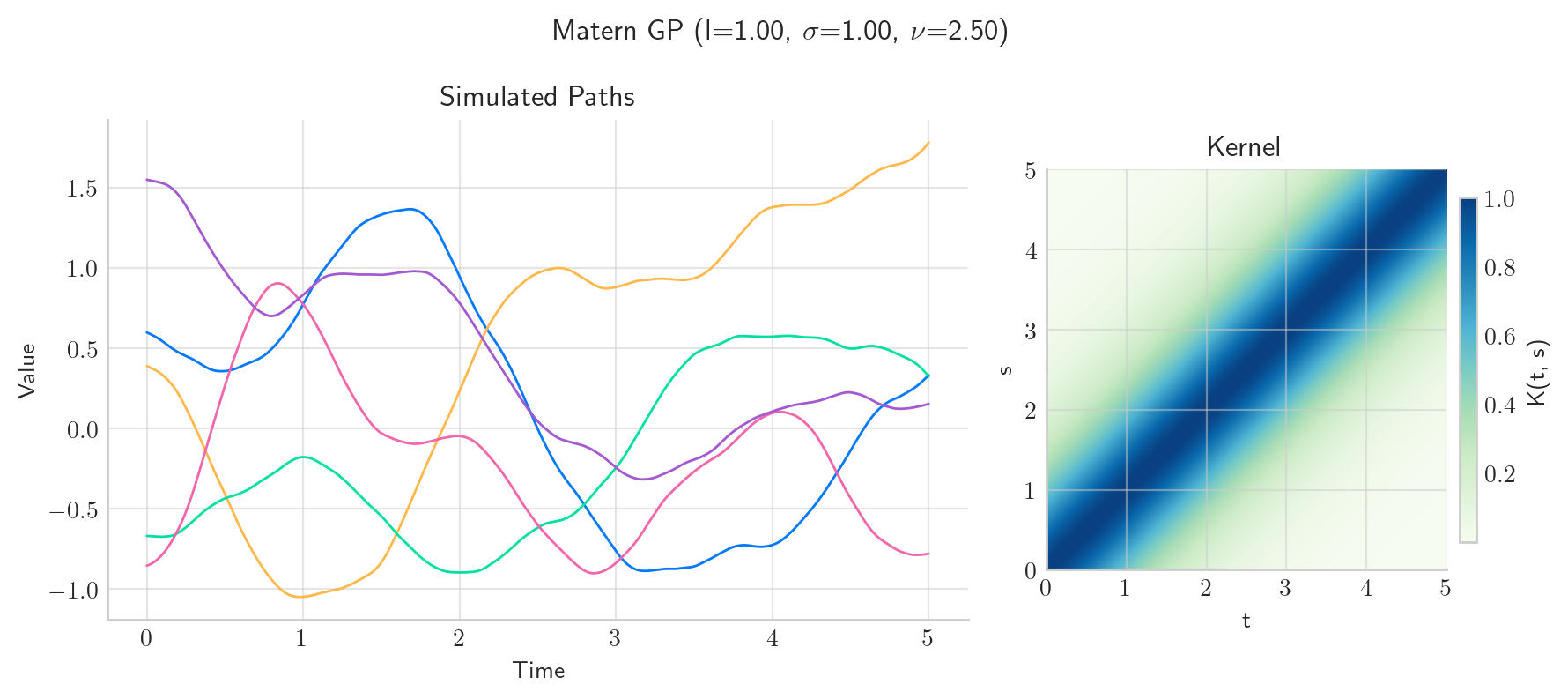

The Matérn class \(k_\nu\) yields sample paths that are \(\lfloor \nu \rfloor\)-times mean-square differentiable; in particular, \(\nu = \tfrac{1}{2}\) corresponds to non-differentiable paths.

This is a fundamental property in applications, as it allows practitioners to encode prior beliefs about the smoothness of the underlying function being modeled.

from aleatory.processes import GPMatern

p = GPMatern(sigma=1.0, length_scale=1.0, nu=0.5, T=5.0)

fig = p.plot_paths_and_kernel(n=300, N=5, cmap="GnBu")

p = GPMatern(sigma=1.0, length_scale=1.0, nu=1.5, T=5.0)

fig = p.plot_paths_and_kernel(n=300, N=5, cmap="GnBu")

p = GPMatern(sigma=1.0, length_scale=1.0, nu=2.5, T=5.0)

fig = p.plot_paths_and_kernel(n=300, N=5, cmap="GnBu")

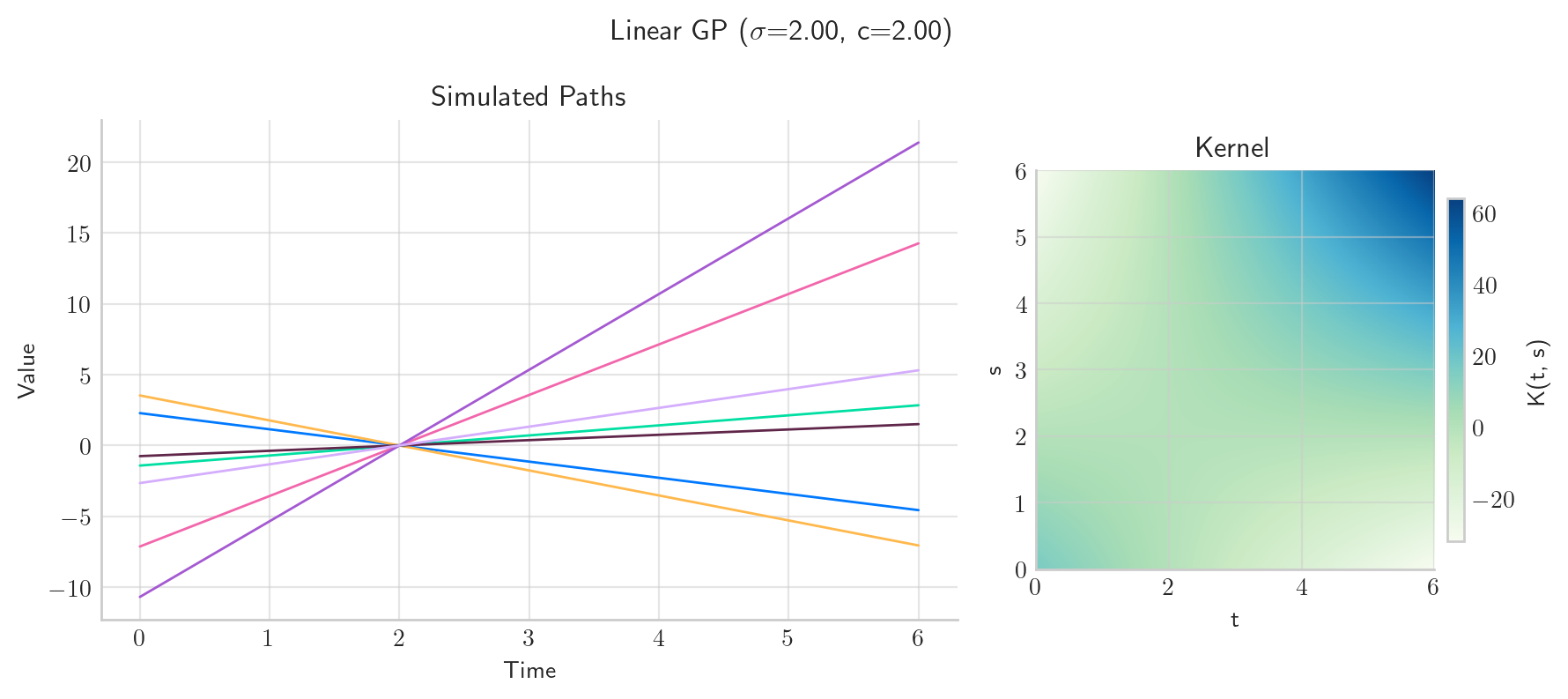

9.7.2. Variability#

Definition: Variability is determined by the pointwise variance of the process, given by

More generally, the covariance function controls the full second-order structure, including how variance is distributed across the index set and how joint fluctuations occur.

Intuition: The magnitude of \(k(t,t)\) sets the scale of fluctuations at each point, while the off-diagonal terms \(k(t,s)\) determine how these fluctuations co-vary. Larger values of \(k(t,t)\) correspond to greater dispersion of the process around its mean.

Examples:

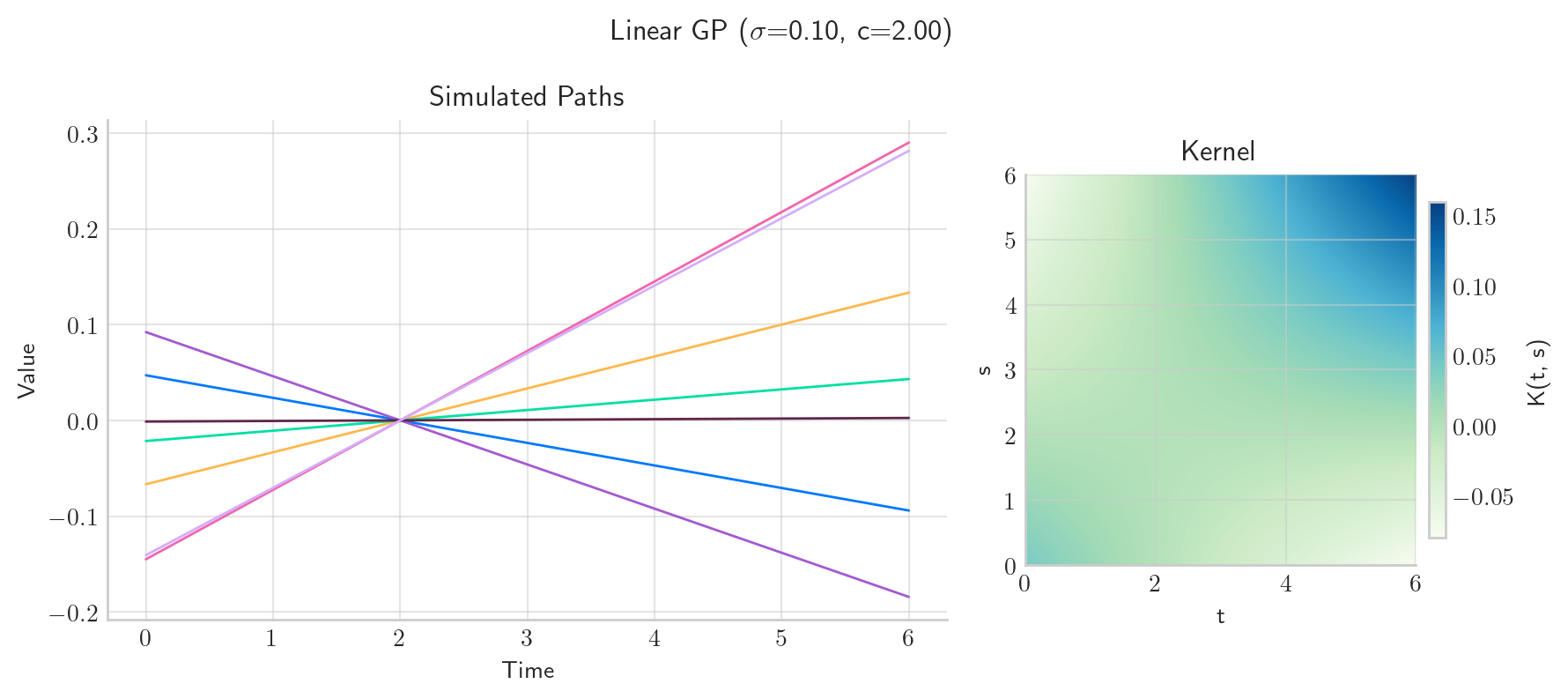

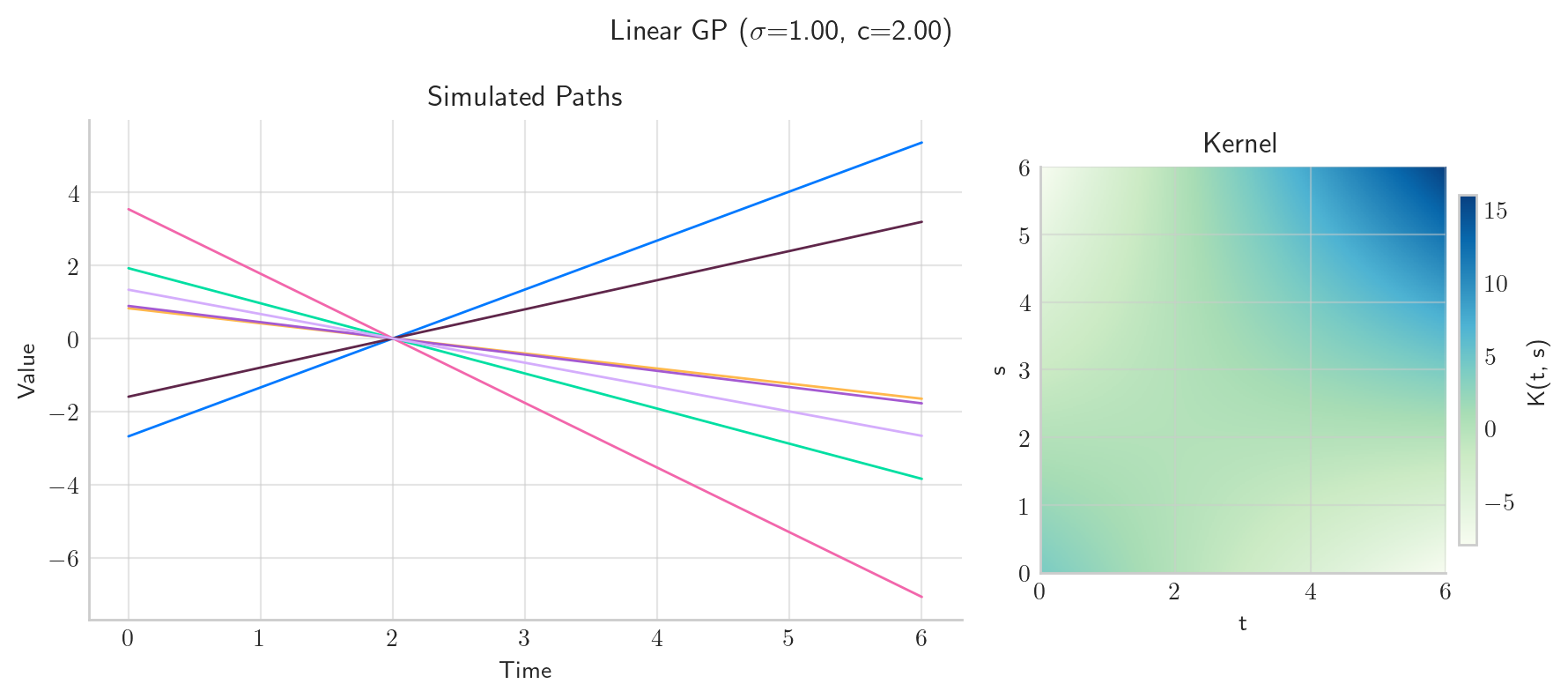

A kernel of the form \(k(t, s) = \sigma^2 \tilde{k}(t,s)\) scales the entire process, with \(\sigma^2\) directly controlling the marginal variance.

In heteroscedastic constructions, one may use \(k(t,s) = \sigma(t)\sigma(s)\tilde{k}(t,s)\), inducing location-dependent variability.

For Brownian motion, \(k(t,t) = t\), so the variance grows linearly in time.

from aleatory.processes import GPLinear

p = GPLinear(sigma=0.1, c=2.0, sigma_b=0.0, T=6.0)

fig = p.plot_paths_and_kernel(n=300, N=7, cmap="GnBu")

p = GPLinear(sigma=1.0, c=2.0, sigma_b=0.0, T=6.0)

fig = p.plot_paths_and_kernel(n=300, N=7, cmap="GnBu")

p = GPLinear(sigma=2.0, c=2.0, sigma_b=0.0, T=6.0)

fig = p.plot_paths_and_kernel(n=300, N=7, cmap="GnBu")

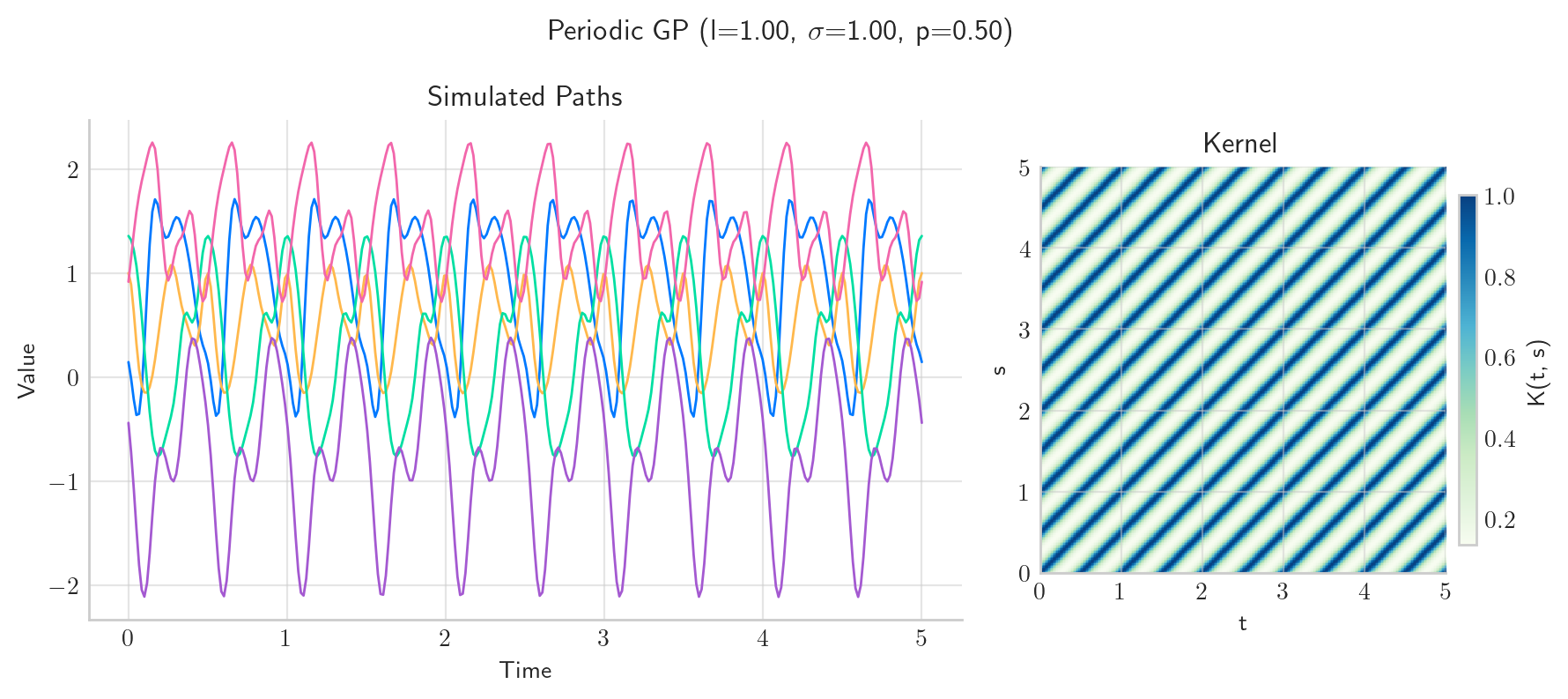

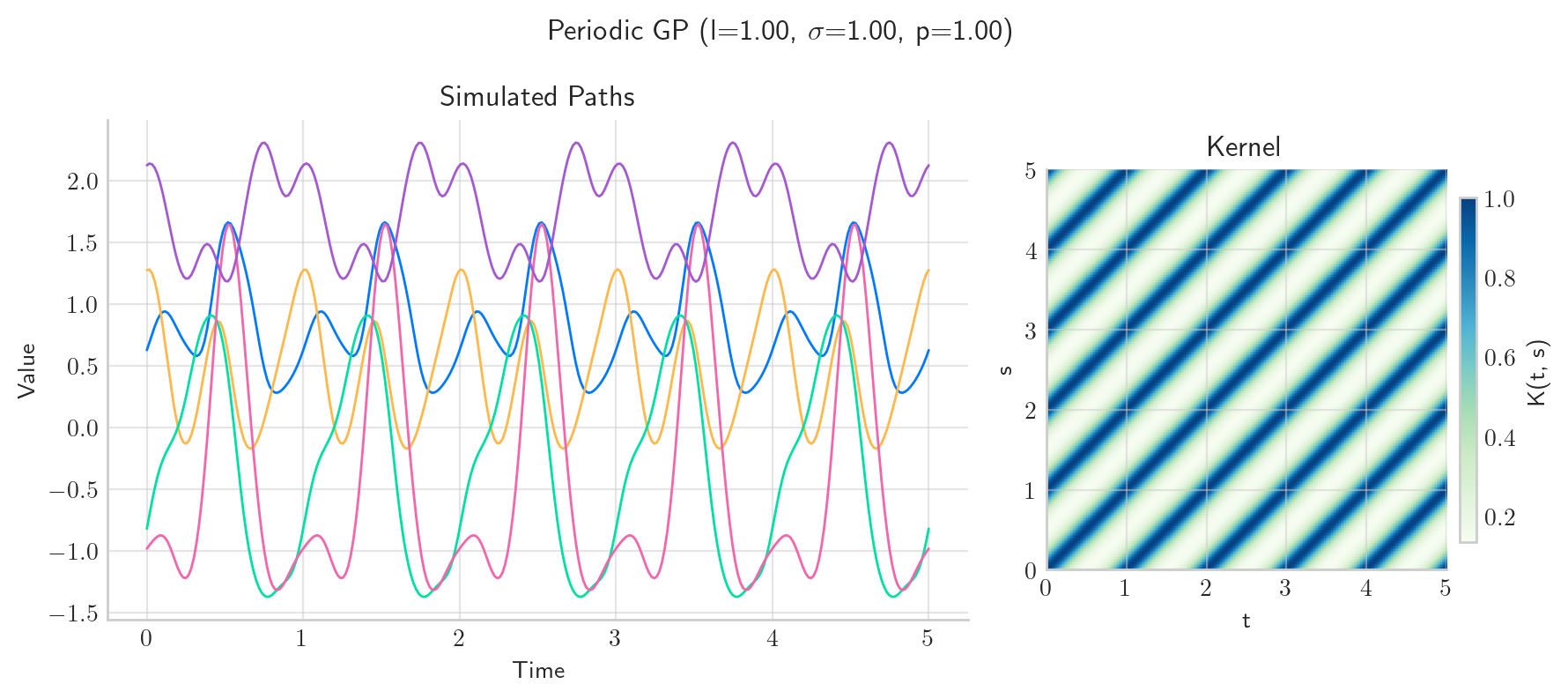

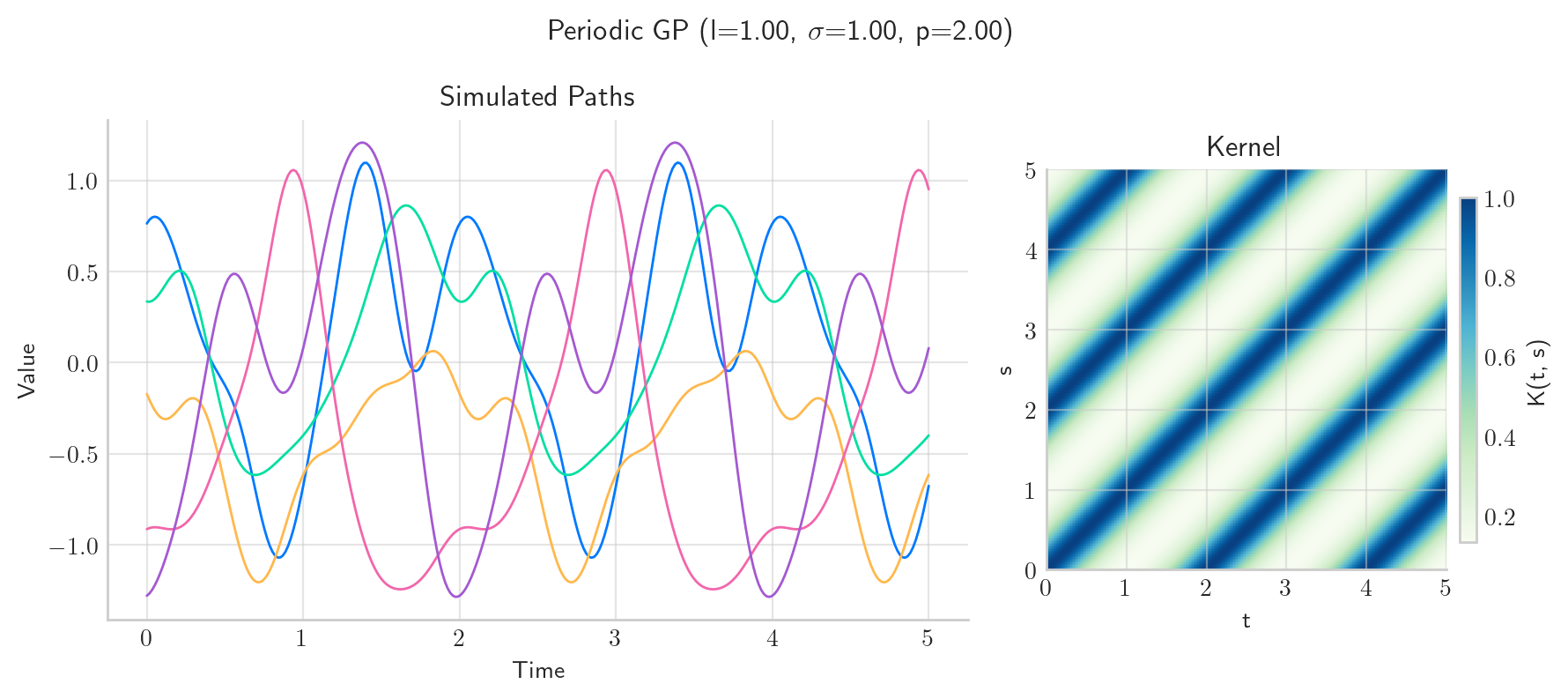

9.7.3. Periodicity#

Definition: A covariance function \(k\) is periodic with period \(T > 0\) if

Equivalently, in the stationary case, periodicity can be expressed as \(k(\tau) = k(\tau + T)\) where \(\tau = t - s\).

Intuition: The covariance structure repeats itself at regular intervals, implying that the dependence between points is invariant under shifts by multiples of the period. This enforces a repeating pattern in the correlation structure of the process.

Examples:

A standard periodic kernel is

which enforces exact periodicity with period \(T\).

Trigonometric covariance functions, such as \(k(\tau) = \cos(2\pi \tau / T)\), generate perfectly periodic structure.

Sums/products of periodic and non-periodic kernels allow periodic behaviour with slowly varying amplitudes.

from aleatory.processes import GPPeriodic

p = GPPeriodic(sigma=1.0, length_scale=1.0, period=0.5, T=5.0)

fig = p.plot_paths_and_kernel(n=300, N=5, cmap="GnBu")

p = GPPeriodic(sigma=1.0, length_scale=1.0, period=1.0, T=5.0)

fig = p.plot_paths_and_kernel(n=300, N=5, cmap="GnBu")

p = GPPeriodic(sigma=1.0, length_scale=1.0, period=2.0, T=5.0)

fig = p.plot_paths_and_kernel(n=300, N=5, cmap="GnBu")

9.7.4. Mean Reversion#

Definition: Mean reversion can be formalized through the decay of covariance over time. A process exhibits mean-reverting behaviour if, for fixed \(s\),

and the decay occurs at a rate that enforces a characteristic timescale of dependence.

Intuition: As the temporal separation increases, the influence of past values on future values diminishes, causing the process to “forget” deviations from the mean and revert toward it. The rate of decay determines how quickly this reversion occurs.

Examples:

The exponential kernel

corresponds to the covariance of the Ornstein–Uhlenbeck process, a canonical mean-reverting model.

More generally, Matérn kernels with finite length scale exhibit mean-reverting behaviour through exponential-type decay.

In contrast, kernels with slow (e.g., polynomial) decay encode long memory and weaker mean reversion.

9.7.5. Stationarity#

Definition: A process \(X\) is (weakly) stationary if its covariance function satisfies

i.e., it depends only on the lag \(\tau = t - s\), and the mean is constant.

Intuition: The statistical structure of the process is invariant under translations of the index set. There is no distinguished location in \(\mathcal{T}\); only relative separation matters.

Examples:

The squared exponential and Matérn kernels are stationary since they depend only on \(t-s\).

A kernel like \(k(t,s) = \min(t,s)\) is non-stationary, as it depends on absolute time.

Adding a non-constant variance term (e.g., \(k(t,s) = t s\)) breaks stationarity.

9.7.6. Isotropy#

Definition: When \(\mathcal{T} \subset \mathbb{R}^d\), a covariance function is isotropic if there exists a function \(\psi : [0,\infty) \to \mathbb{R}\) such that

where \(|\cdot|\) is the Euclidean norm.

Intuition: The dependence between two points depends only on the distance between them, not on the direction. The process exhibits rotational invariance in its covariance structure.

Examples:

The radial basis function kernel \(k(t,s) = \sigma^2 \exp(-|t-s|^2 / (2\ell^2))\) is isotropic.

Anisotropic kernels take the form \(k(t,s) = \exp\big(-(t-s)^\top \Lambda^{-1} (t-s)\big)\), where \(\Lambda\) introduces direction-dependent scaling.

In spatial statistics, isotropic kernels assume uniform behaviour in all directions, while anisotropic ones capture directional effects such as prevailing winds or geological structure.

These examples illustrate how specific functional forms of the covariance function translate directly into qualitative properties of the stochastic process.

9.8. Further Reading#

Rasmussen, C. E., & Williams, C. K. I. (2006). Gaussian Processes for Machine Learning. MIT Press.

Murphy, K. P. (2012). Machine Learning: A Probabilistic Perspective. MIT Press.