Day 24: Fractional Brownian motion#

Fractional Brownian Motion (fBm) is a generalisation of classical Brownian motion introduced to model complex phenomena exhibiting long-range dependence and self-similarity. Since its inception, fBm has become a cornerstone in fields like finance, physics, and telecommunications.

Definition#

The fractional Brownian motion (fBM) is a continuous-time Gaussian process \(B\_H(t)\) on \(\[0,T\]\) that starts at zero, has expectation zero for all \(t\) in \(\[0,T\]\), and has the following covariance function:

where H is a real number in (0, 1), called the Hurst index or Hurst parameter associated with the fractional Brownian motion. The value of H determines what kind of process the fBm is:

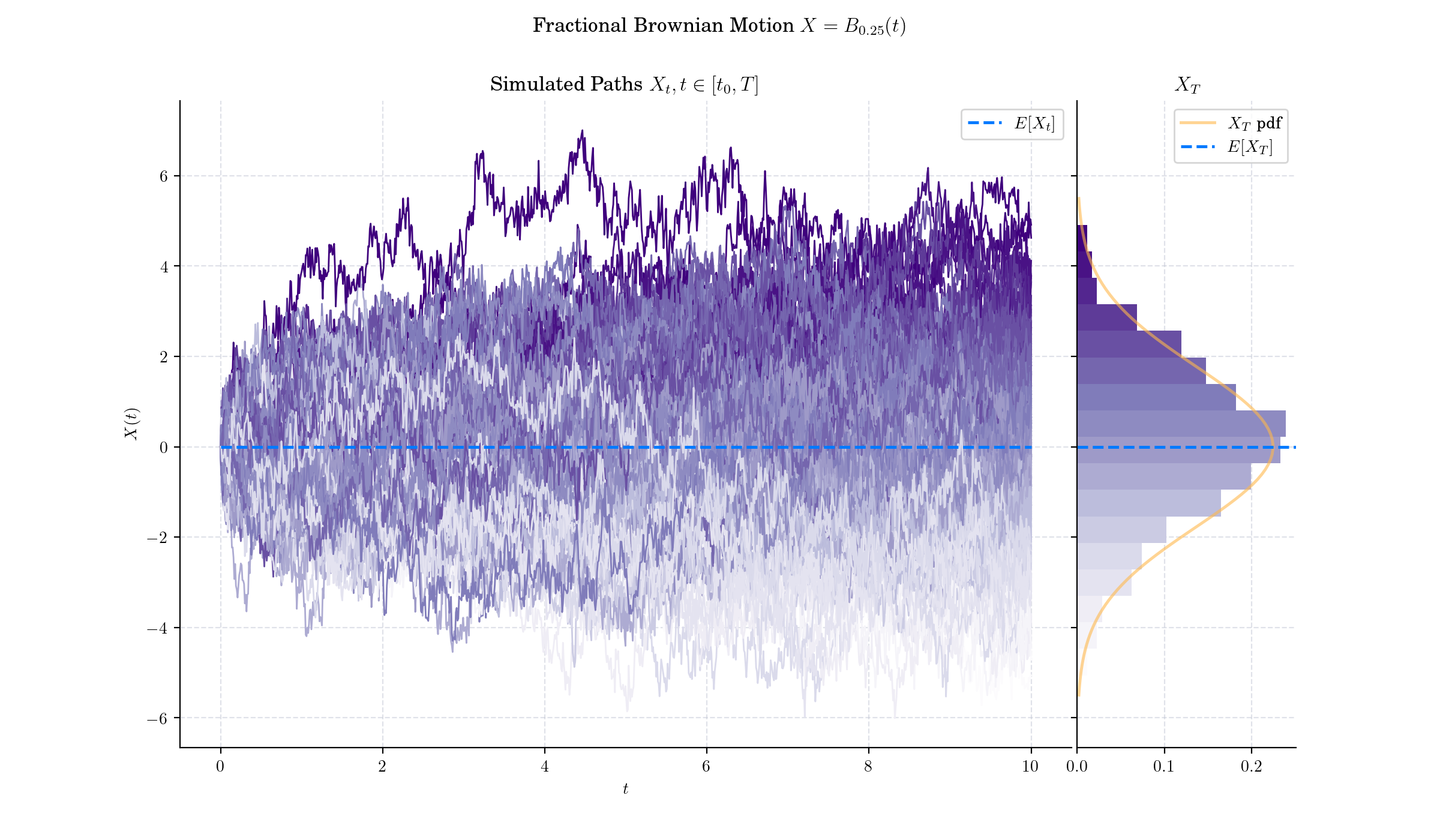

if H < 1/2 then the increments of the process are negatively correlated.

if H = 1/2 then the process is in fact a Brownian motion or Wiener process;

if H > 1/2 then the increments of the process are positively correlated;

🔔 Random Facts 🔔#

Although the main principles of fBM were introduced earlier by Kolmogorov, the name was introduced by Mandelbrot and van Ness (1968) who defined the process as a stochastic integral

The Hurst exponent describes the raggedness of the resultant motion, with a higher value leading to a smoother motion. It was introduced by Mandelbrot & van Ness (1968).

There is a generalisation of fractional Brownian motion: n-th order fractional Brownian motion, abbreviated as n-fBm. n-fBm is a Gaussian, self-similar, non-stationary process whose increments of order \(n\) are stationary.

The main difference between fractional Brownian motion and regular Brownian motion is that while the increments in Brownian Motion are independent, increments for fractional Brownian motion are not.

Various methods have been developed to generate samples of fBm efficiently. To produce our visualisations we use the Davies-Harte method which relies on the Fast Fourier Transform (FFT) and is computationally efficient with complexity \(O(n log(n))\).

More to Read 📚#

Mandelbrot, Benoit B., and John W. Van Ness. “Fractional Brownian Motions, Fractional Noises and Applications.” SIAM Review, vol. 10, no. 4, 1968, pp. 422–37. JSTOR, http://www.jstor.org/stable/2027184.

Davies, R. B., and D. S. Harte. “Tests for Hurst Effect.” Biometrika, vol. 74, no. 1, 1987, pp. 95–101. JSTOR, https://doi.org/10.2307/2336024.

Sainty, P. (1992), “Construction of a complex-valued fractional Brownian motion of order N”, Journal of Mathematical Physics, 33 (9): 3128, Bibcode:1992JMP….33.3128S, doi:10.1063/1.529976

P.s. If you are curious about probability distributions visit the Advent Calendar 2023 ✨