Day 13 : Exponential#

The exponential distribution or negative exponential distribution is the probability distribution of the time between events in a Poisson point process, i.e., a process in which events occur continuously and independently at a constant average rate. It has support \([0, \infty)\) and is defined by a parameter \(\lambda>0\) which is called rate (or inverse scale).

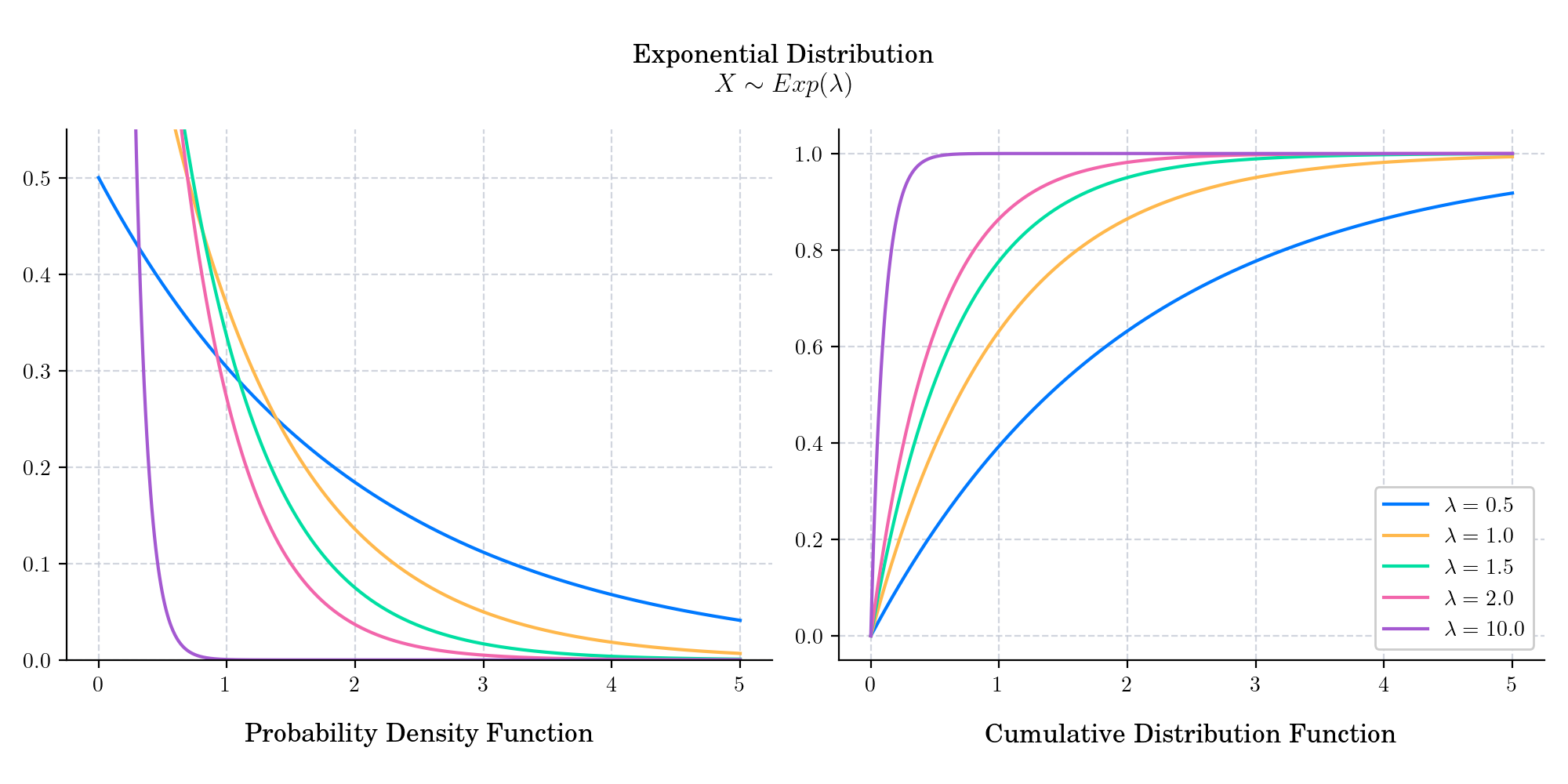

The probability density function is given by

The cumulative distribution function is given by

🔔 Random Facts 🔔#

An exponentially distributed random variable \(T\sim Exp(\lambda)\) obeys the relation \(P(T>s+t| T>s) = P(T>t)\). This property is known as memorylessness.

The exponential distribution and the geometric distribution are the only memoryless probability distributions. The exponential distribution is consequently also necessarily the only continuous probability distribution that has a constant failure rate.

If X ~ Pareto(1, λ), then log(X) ~ Exp(λ).

In physics it is often used to measure radioactive decay, in engineering it is used to measure the time associated with receiving a defective part on an assembly line, and in finance it is often used to measure the likelihood of the next default for a portfolio of financial assets. It can also be used to measure the likelihood of incurring a specified number of defaults within a specified time period.