Note

Go to the end to download the full example code.

Black Monday#

# Author: Dialid Santiago <d.santiago@outlook.com>

# License: MIT

# Description: Advent Calendar 2025 Day 5 - Black Monday Crash

import yfinance as yf

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import norm

plt.style.use("https://raw.githubusercontent.com/quantgirluk/matplotlib-stylesheets/main/quant-pastel-light.mplstyle")

ticker = "^GSPC"

data = yf.download(ticker, start="1985-01-01", progress=False, auto_adjust=False)

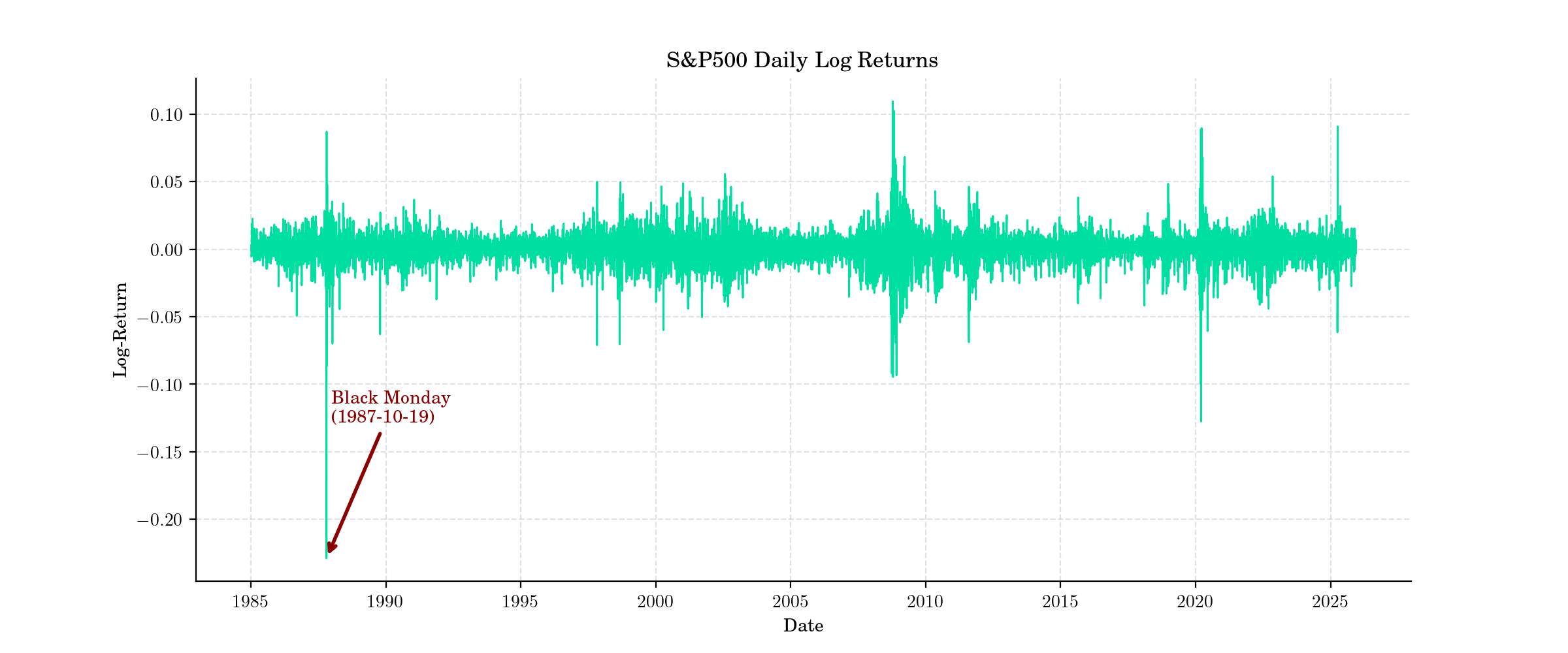

black_monday_date = pd.Timestamp('1987-10-19')

# Close prices

prices = data["Close"]

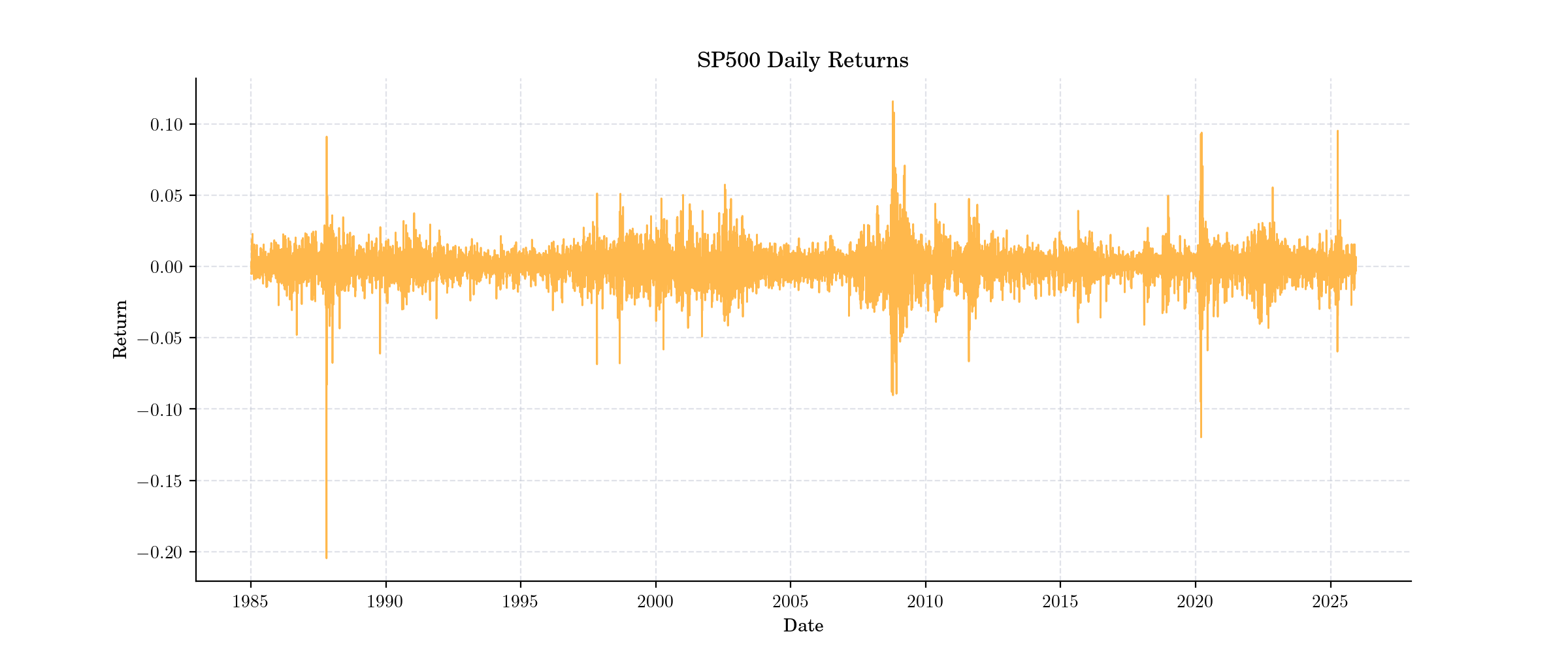

# Simple returns

returns = prices.pct_change()

# Logarithmic returns

log_returns = np.log(prices / prices.shift(1))

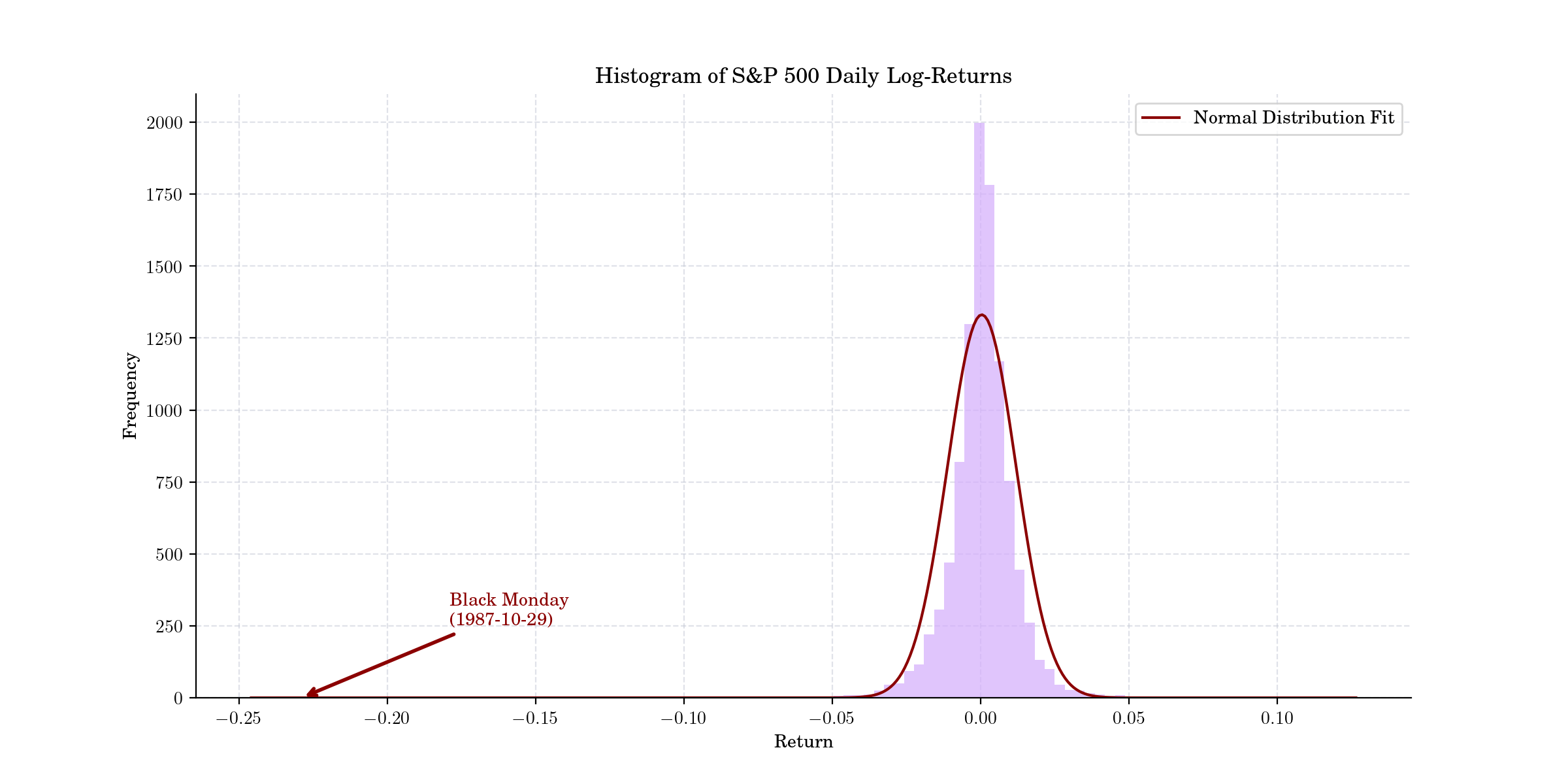

mean = log_returns.mean()

std = log_returns.std()

x = log_returns[log_returns.index == black_monday_date][ticker]

black_monday_log_return = x.values[0]

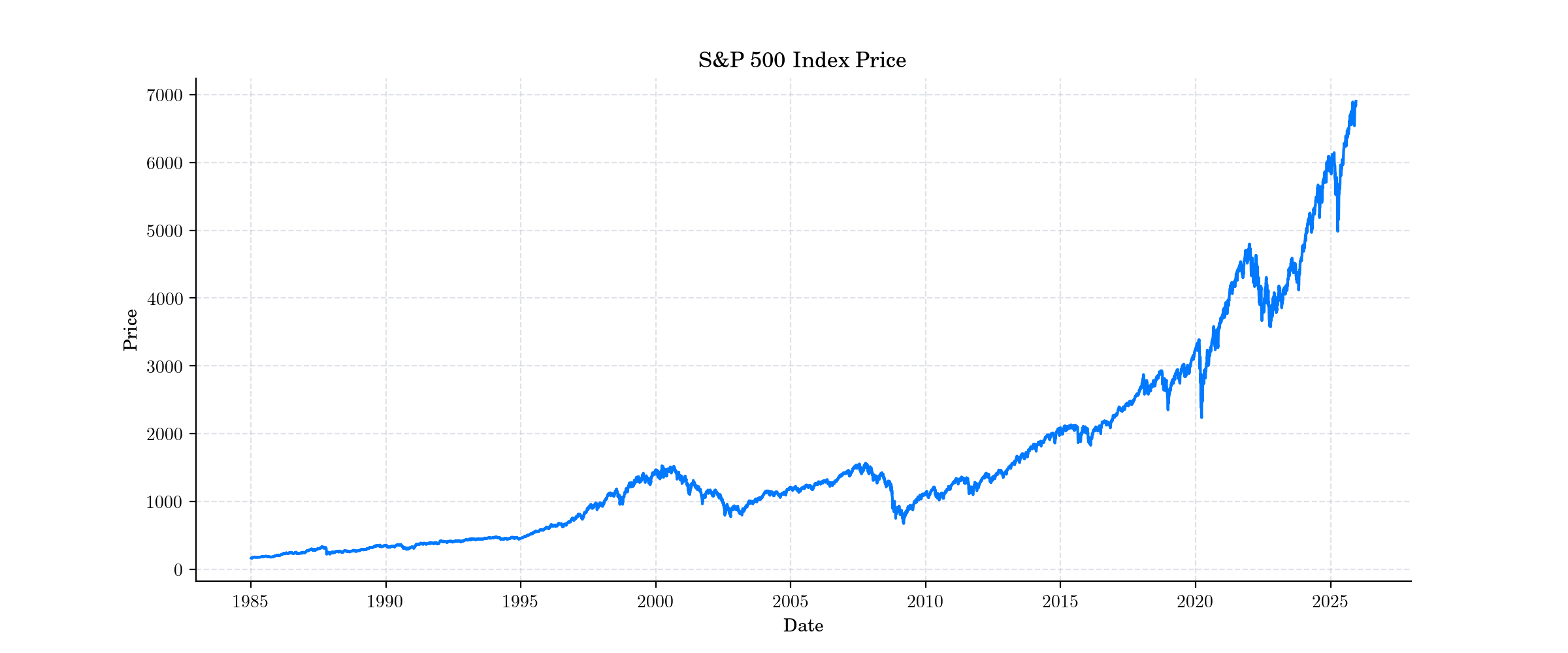

plt.figure(figsize=(12, 5), dpi=200)

plt.plot(prices, color='#0079ff', linewidth=1.5)

plt.title("S\\&P 500 Index Price")

plt.xlabel("Date")

plt.ylabel("Price")

plt.grid(True)

plt.show()

plt.figure(figsize=(12, 5), dpi=200)

plt.plot(returns, color='#ffb84c')

plt.title("SP500 Daily Returns")

plt.xlabel("Date")

plt.ylabel("Return")

plt.grid(True)

plt.show()

plt.figure(figsize=(12, 5), dpi=200)

plt.plot(log_returns, color='#00dfa2')

if not np.isnan(black_monday_log_return):

plt.annotate(

'Black Monday\n(1987-10-19)',

xy=(black_monday_date ,black_monday_log_return),

xytext=(pd.Timestamp('1987-12-19'), black_monday_log_return + 0.1),

arrowprops=dict(arrowstyle='->', color='darkred', lw=2),

fontsize=10,

ha='left',

color='darkred',

weight='bold'

)

plt.title("S\\&P500 Daily Log Returns")

plt.xlabel("Date")

plt.ylabel("Log-Return")

plt.grid(True)

plt.show()

plt.figure(figsize=(12, 6), dpi=200)

plt.hist(log_returns.dropna(), bins=100, color='#d4Adfc', alpha=0.7)

xmin, xmax = plt.xlim()

x = np.linspace(xmin, xmax, 400)

p = norm.pdf(x, mean, std)

plt.plot(x, p * len(log_returns.dropna()) * (xmax - xmin) / 100, 'darkred', linewidth=1.5, label='Normal Distribution Fit')

if not np.isnan(black_monday_log_return):

plt.annotate(

'Black Monday\n(1987-10-29)',

xy=(black_monday_log_return, 0),

xytext=(black_monday_log_return + 0.05, 250),

arrowprops=dict(arrowstyle='->', color='darkred', lw=2),

fontsize=10,

ha='left',

color='darkred',

weight='bold'

)

plt.title("Histogram of S\\&P 500 Daily Log-Returns")

plt.xlabel("Return")

plt.ylabel("Frequency")

plt.legend()

plt.show()

Total running time of the script: (0 minutes 8.555 seconds)