Note

Go to the end to download the full example code.

Returns and Log-Returns#

# Author: Dialid Santiago <d.santiago@outlook.com>

# License: MIT

# Description: Advent Calendar 2025 Day 5 - Plotting Returns of S&P 500

import yfinance as yf

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

quant_pastel = "https://raw.githubusercontent.com/quantgirluk/matplotlib-stylesheets/main/quant-pastel-light.mplstyle"

plt.style.use(quant_pastel)

plt.rc('font', family='sans-serif')

plt.rc('font', serif='Apple SD Gothic Neo')

plt.rcParams.update({'font.size': 12})

# ---------------------------------------------------------

# 1. Download S&P 500 Daily Prices from Yahoo Finance

# ---------------------------------------------------------

ticker = "^GSPC"

data = yf.download(ticker, start="2000-01-01", progress=False, auto_adjust=False)

prices = data["Close"]

# ---------------------------------------------------------

# 2. Compute Returns

# ---------------------------------------------------------

returns = prices.pct_change()

log_returns = np.log(prices / prices.shift(1))

# ---------------------------------------------------------

# 3. Multi-panel Figure

# ---------------------------------------------------------

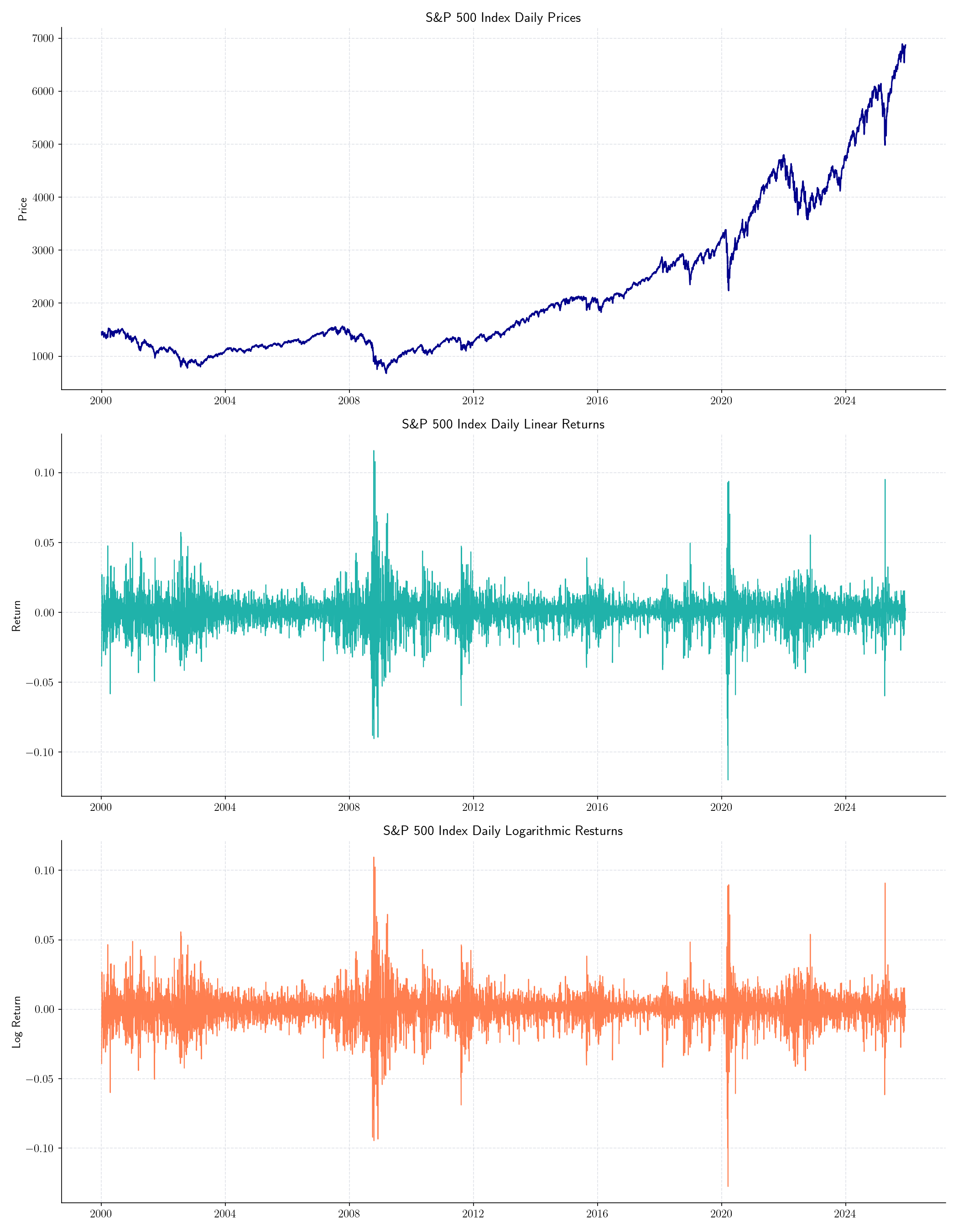

fig, axes = plt.subplots(3, 1, figsize=(14, 18), sharex=False, dpi=150)

# Price

axes[0].plot(prices, color='darkblue', linewidth=1.5)

axes[0].set_title("S\\&P 500 Index Daily Prices")

axes[0].set_ylabel("Price")

axes[0].grid(True)

# Returns

axes[1].plot(returns, color='lightseagreen')

axes[1].set_title("S\\&P 500 Index Daily Linear Returns")

axes[1].set_ylabel("Return")

axes[1].grid(True)

# Log Returns

axes[2].plot(log_returns, color='coral')

axes[2].set_title("S\\&P 500 Index Daily Logarithmic Resturns")

axes[2].set_ylabel("Log Return")

axes[2].grid(True)

plt.tight_layout()

plt.show()

# Histogram and box plot of returns

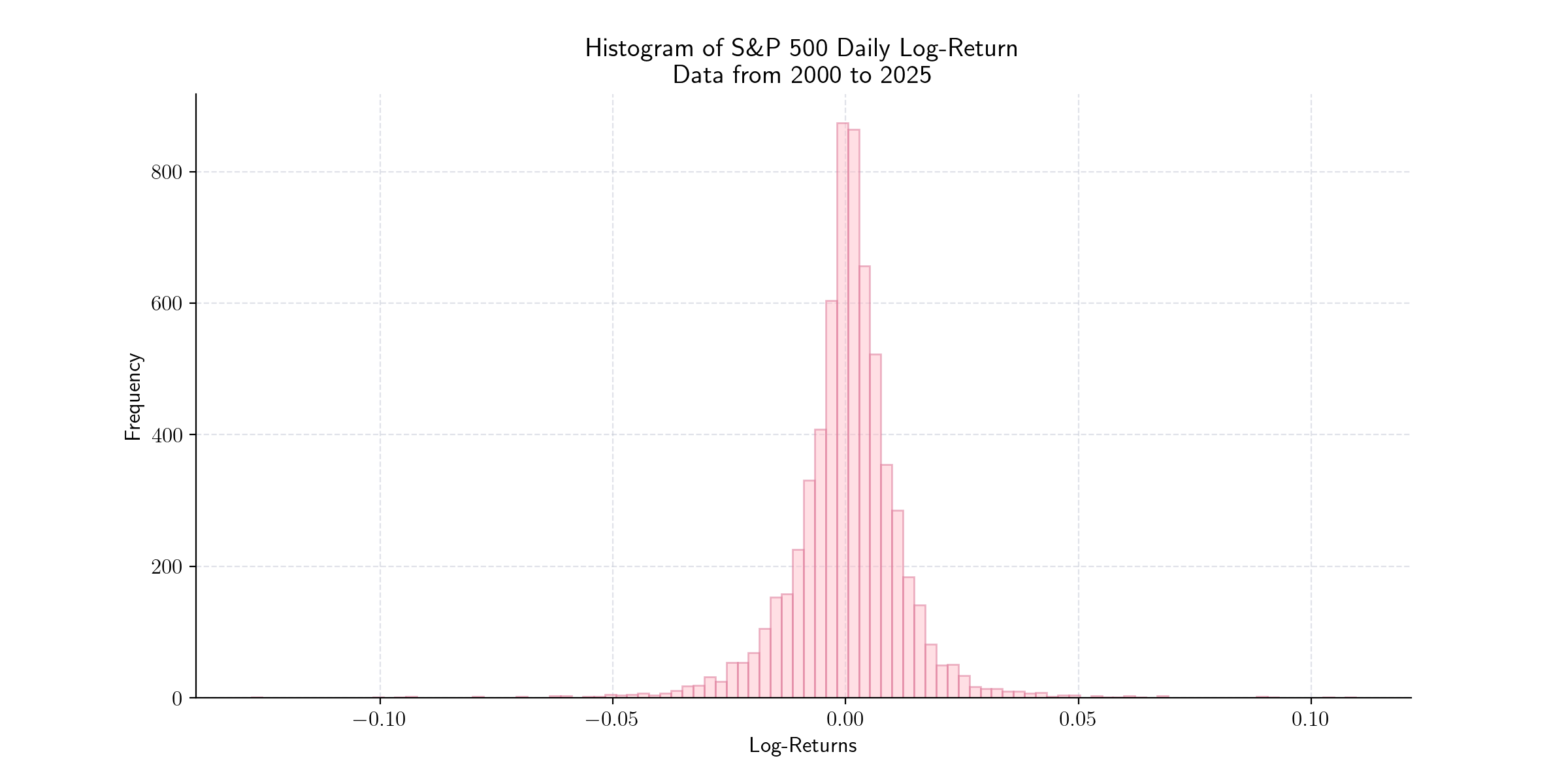

plt.figure(figsize=(12, 6), dpi=200)

plt.hist(log_returns.dropna(), bins=100, alpha=0.5, color='pink', edgecolor='palevioletred')

plt.title("Histogram of S\\&P 500 Daily Log-Return\n Data from 2000 to 2025",)

plt.xlabel("Log-Returns")

plt.ylabel("Frequency")

plt.show()

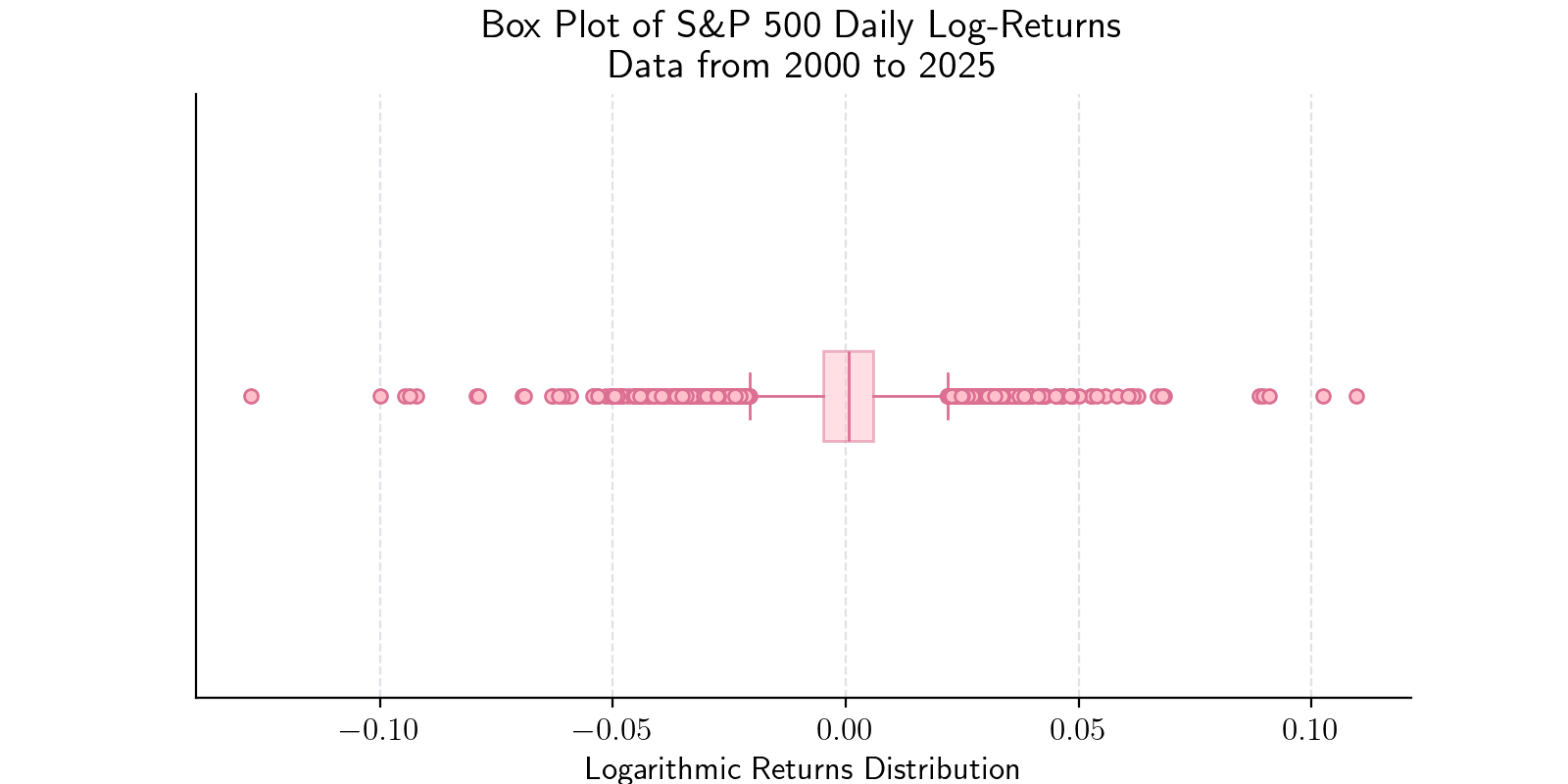

plt.figure(figsize=(8, 4), dpi=200)

plt.boxplot(

log_returns.dropna(),

orientation='horizontal',

patch_artist=True,

boxprops=dict(edgecolor='palevioletred', facecolor='pink', alpha=0.5),

medianprops=dict(color='palevioletred'),

whiskerprops=dict(color='palevioletred'),

capprops=dict(color='palevioletred'),

flierprops=dict(marker='o', markerfacecolor='pink', markeredgecolor='palevioletred', markersize=5)

)

plt.yticks([])

plt.title("Box Plot of S\\&P 500 Daily Log-Returns\n Data from 2000 to 2025")

plt.xlabel("Logarithmic Returns Distribution")

plt.grid(True)

plt.show()

Total running time of the script: (0 minutes 6.276 seconds)